Updated: May 14, 2026

Executive Summary

Most people compare Medicare choices and costs by looking first at the monthly premium. That is understandable, but it is also where many bad Medicare decisions begin.

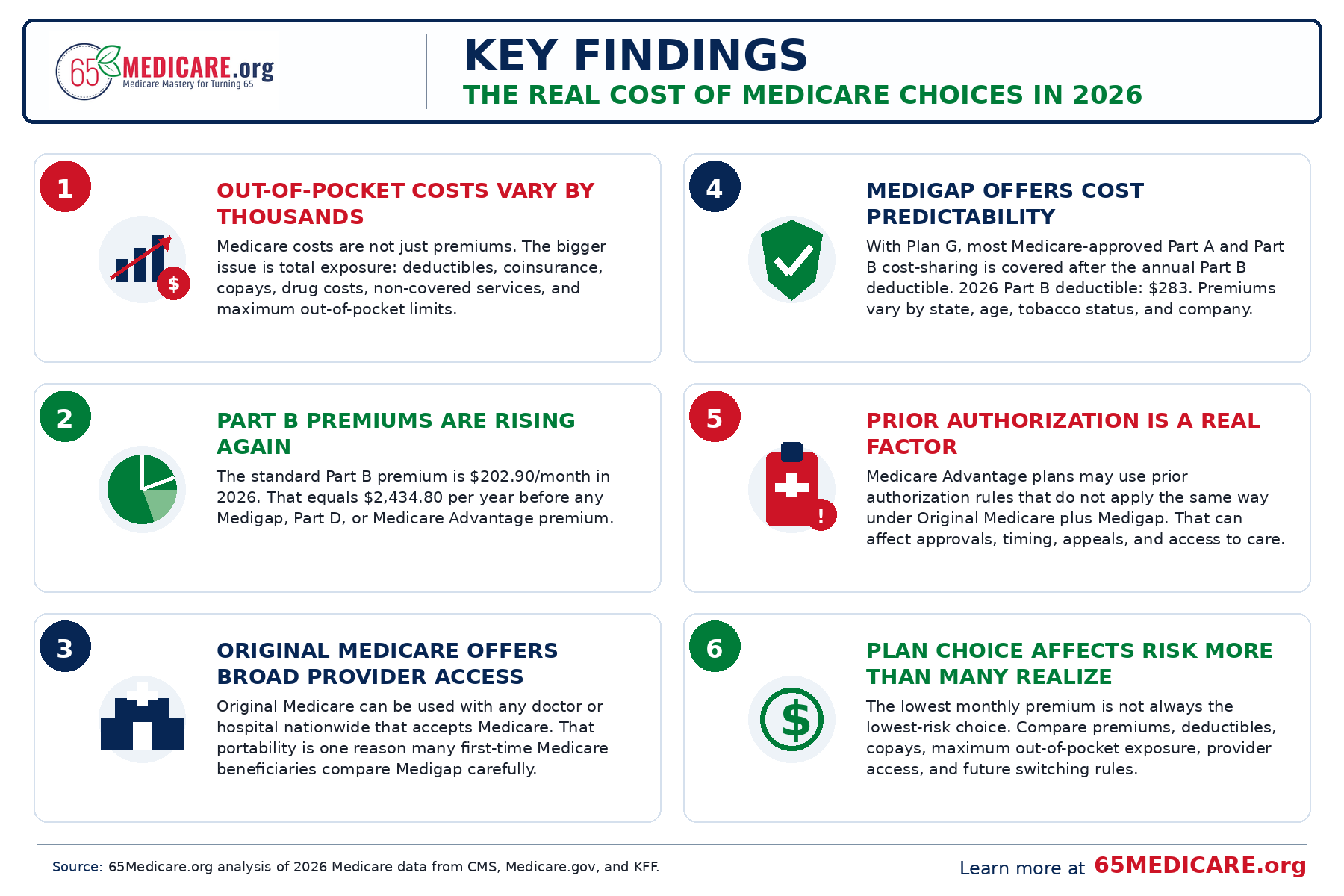

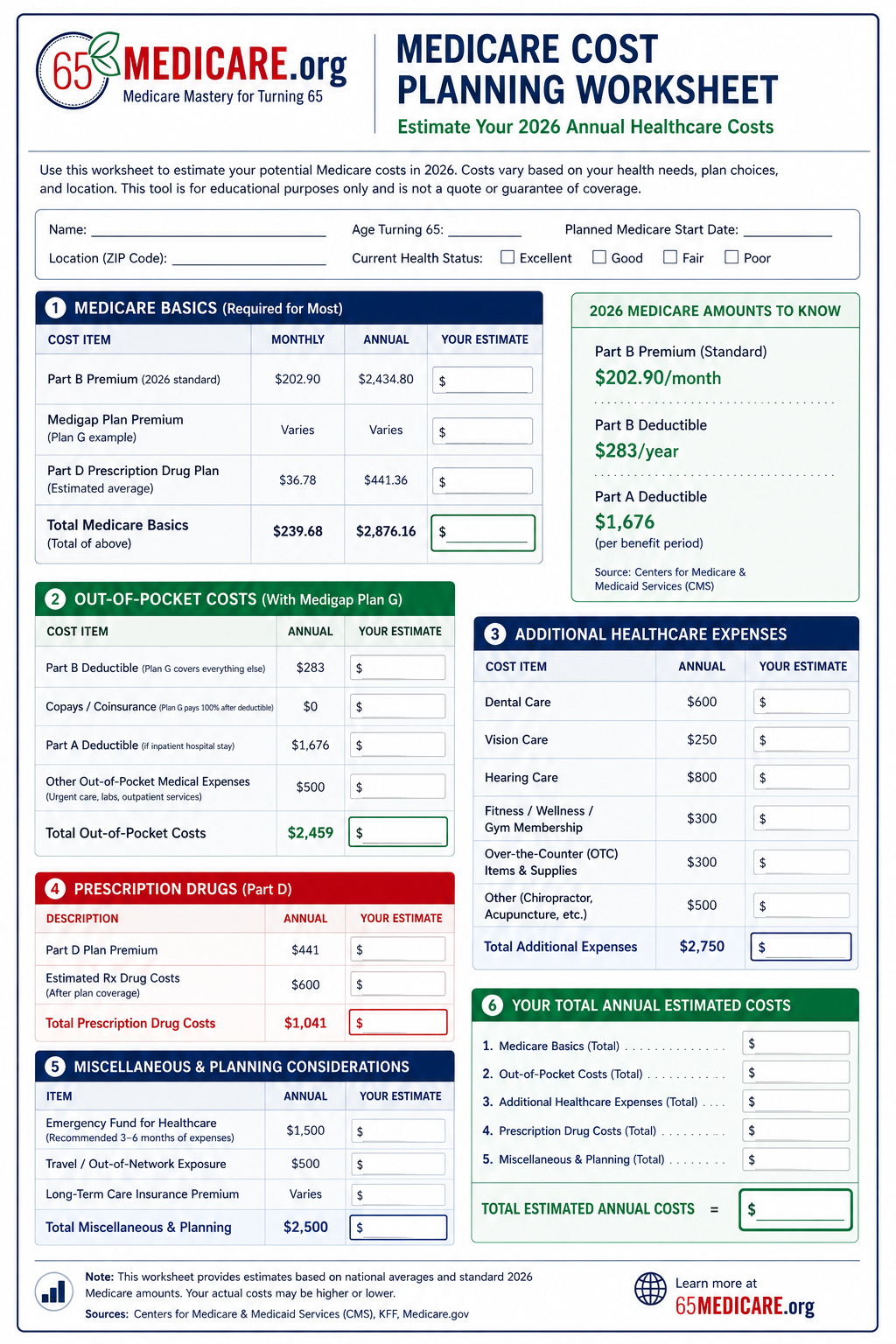

In 2026, the standard Medicare Part B premium is $202.90 per month and the Part B deductible is $283. Those amounts apply whether a person chooses Original Medicare with a Medigap policy or enrolls in a Medicare Advantage plan. From there, the real cost picture changes dramatically based on how the person receives care, how often they travel, what doctors they use, which prescriptions they take, and whether they want predictable costs or lower monthly premiums with more cost-sharing later.

The central finding of this 65Medicare.org study is simple: the true Medicare costs are not just premiums. It is the combination of premiums, deductibles, copays, coinsurance, prescription costs, provider access, plan rules, and future flexibility.

That distinction matters most for people turning 65. This is often the one point in life when a person can compare Medicare options with the broadest set of choices. After the first enrollment window passes, changing from one Medicare path to another may not be equally easy in every direction.

- Original Medicare alone has no built-in annual out-of-pocket maximum for Part A and Part B services.

- Medigap can make Original Medicare much more predictable by helping pay Medicare deductibles, copays, and coinsurance.

- Medicare Advantage plans often have lower monthly premiums, and many include extra benefits, but they also use plan-specific networks, cost-sharing, prior authorization, and annual out-of-pocket limits.

- Part D drug costs can change the answer for either path.

- Provider access should be treated as a cost issue, not merely a convenience issue.

For readers who are just beginning, start with our Turning 65 Medicare Guide. For a deeper comparison of supplement options, see Medigap Plans: Costs, Coverage, and How to Choose the Best Plan.

Methodology: How This Study Was Built

This study is a practical cost analysis, not a carrier ranking. We reviewed national Medicare costs data for 2026, public Medicare.gov explanations of Medigap and Medicare Advantage, KFF reporting on Medicare Advantage plan availability and premiums, and public reporting on prior authorization trends.

We intentionally did not rank specific insurance companies in this article. Carrier pricing changes by state, county, ZIP code, age, tobacco status, household discount eligibility, and underwriting rules. A national article that pretends one company is best everywhere would be less helpful, not more helpful.

Instead, this study focuses on the decision structure: what costs are predictable, what costs are variable, what costs are hidden until a person uses care, and what tradeoffs matter most when someone is starting Medicare for the first time.

Throughout the article, the word ‘Medigap’ refers to Medicare Supplement Insurance that works with Original Medicare. The term ‘Medicare Advantage’ refers to private Medicare plans that replace the way a person receives Part A and Part B benefits for the year they are enrolled.

What We Mean by the ‘Real Costs’ of Medicare

The real cost of Medicare is the amount a person is likely to pay in a normal year, plus the amount they could reasonably be exposed to in a bad health year.

That definition is more useful than premium-only shopping. A healthy 65-year-old may look at two choices and see one with a higher monthly premium and one with a lower monthly premium. In a normal year, the lower-premium choice may look attractive. But Medicare choices are not only a normal-year decision. It is also a decision about what happens if that person has surgery, starts seeing several specialists, receives outpatient therapy, needs expensive imaging, develops a chronic condition, or spends several months away from home.

For that reason, this analysis evaluates Medicare costs across six categories: premiums, deductibles, copays, coinsurance, drug costs, and access-related costs. Access-related costs include the financial consequences of networks, prior authorization, referrals, travel limitations, and the ability or inability to switch coverage later.

This is why two reasonable people can choose different Medicare paths. A person who wants the lowest monthly premium and is comfortable with a local network may view Medicare Advantage differently from a person who wants nationwide provider access and predictable medical bills. A person with no prescriptions may view Part D differently from someone taking several brand-name drugs.

Key 2026 Medicare Cost Numbers

The following national figures are useful starting points. Some are set nationally by Medicare. Others vary by plan, location, insurance company, and prescription list.

| Cost item | 2026 amount | Why it matters |

| Part B standard premium | $202.90/month | Usually paid regardless of whether someone chooses Original Medicare + Medigap or Medicare Advantage. |

| Part B deductible | $283/year | Applies before Part B generally begins paying its share for many outpatient services. |

| Part A inpatient hospital deductible | $1,736 per benefit period | Can apply when admitted as an inpatient; it is not an annual deductible. |

| Part B coinsurance | Generally 20% after deductible | Original Medicare alone leaves the beneficiary exposed to ongoing coinsurance. |

| Medicare Advantage average premium | $14/month estimated average for 2026 | Many plans have $0 additional premium, but cost-sharing and network rules still matter. |

| Medigap premium | Varies by state, age, ZIP code, tobacco status, household discount, and company | Medigap creates more predictable medical costs, but the monthly premium must be compared carefully. |

| Part D prescription drug coverage | Plan-specific premiums, formularies, and pharmacies | Drug costs can change the best plan decision even when medical coverage looks similar. |

Finding 1: Premiums Are Only the Beginning

It is easy to understand why people focus on the premium. The premium is visible. It shows up every month. It feels like the price tag.

But Medicare costs do not work like a simple subscription. A plan with a lower premium may still have copays for primary care, specialists, emergency room visits, hospital stays, outpatient procedures, durable medical equipment, physical therapy, chemotherapy, and other services. A plan with a higher premium may reduce or nearly eliminate many of those unpredictable charges.

This is the first decision point for someone starting Medicare: do you want to pay more in fixed premium for more predictable medical costs, or pay less in premium and accept more variability when you use care?

Neither answer is automatically wrong. The mistake is pretending that the premium alone answers the question.

This is why our Medigap Plan G overview and Medigap Plan N overview are two of the most important pages for new Medicare beneficiaries. Plan G is often the predictable-cost benchmark, while Plan N is often considered by people who are willing to accept some cost-sharing in exchange for a lower premium.

Finding 2: Original Medicare Alone Leaves Open-Ended Medical Exposure

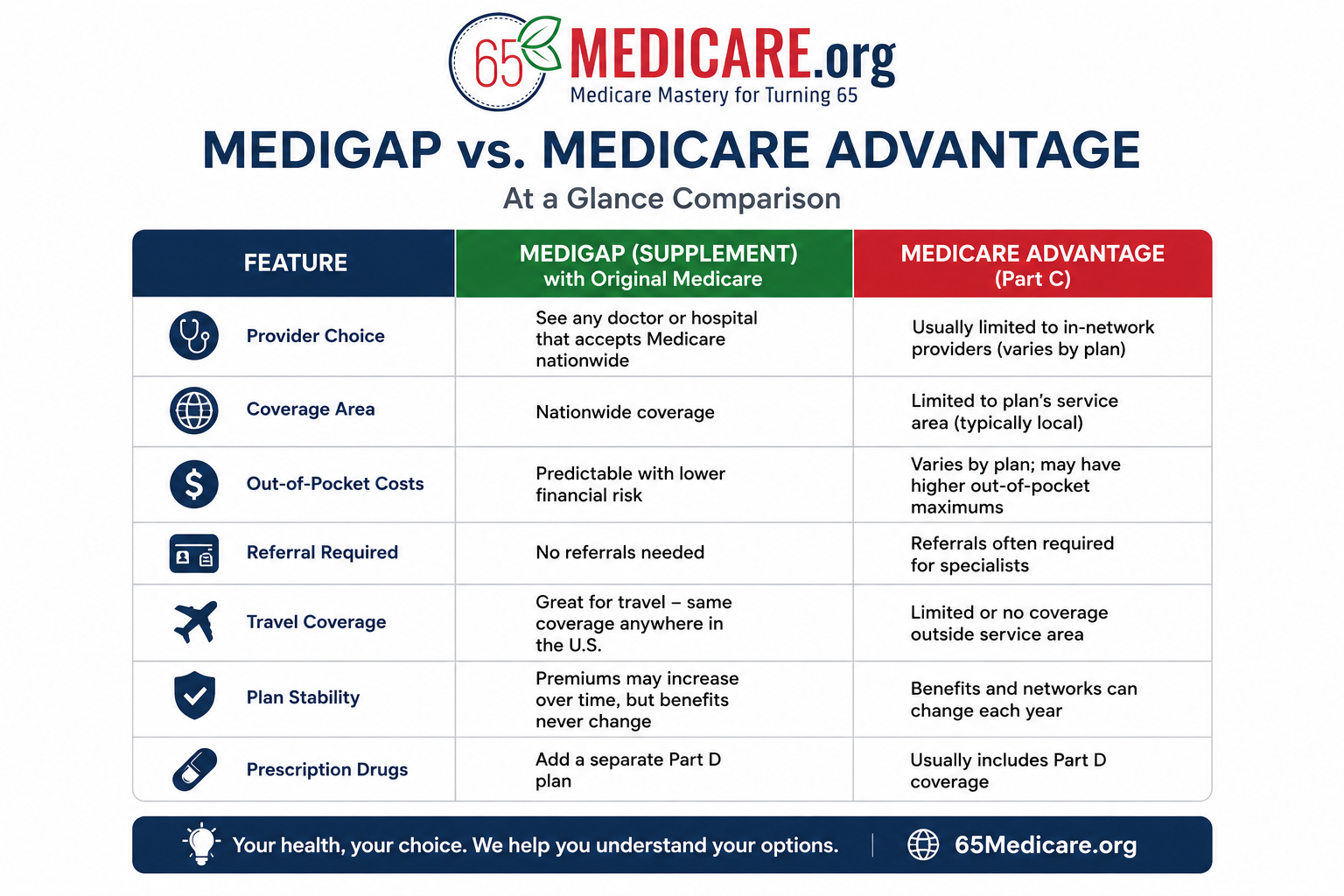

Original Medicare is the foundation of coverage for most people starting Medicare. It is accepted by a very large share of doctors and hospitals, generally does not require a primary care referral to see a specialist, and is not built around a local HMO or PPO network in the same way many Medicare Advantage plans are.

But Original Medicare by itself has a major limitation: it does not include a built-in annual out-of-pocket maximum for Part A and Part B services. That means the 20% Part B coinsurance is not just a theoretical number. For outpatient surgery, cancer treatment, infusion therapy, durable medical equipment, imaging, and specialist-heavy care, that 20% share can become significant.

This is the main reason Medigap exists. Medigap does not replace Medicare. It works with Original Medicare and helps pay some or all of the beneficiary’s share of approved Medicare costs, depending on the plan letter selected.

For a plain-English explanation of how these policies work, see What Is Medigap? and our broader Medigap plans guide.

Finding 3: Medigap Is Best Understood as Cost Predictability

Medigap is often described as supplemental insurance, which is accurate, but incomplete. For many people, the better way to think about Medigap is cost predictability.

With Original Medicare and a strong Medigap plan, the beneficiary is typically choosing to pay a separate monthly premium in exchange for fewer surprises when medical care is needed. That can be especially valuable for someone who wants access to any doctor or hospital that accepts Medicare, travels frequently, lives in more than one state during the year, or simply does not want to compare networks every year.

Medigap plans are standardized by letter in most states. A Plan G from one company provides the same basic medical benefits as a Plan G from another company, even though premiums can vary significantly. Once the plan letter is chosen, the main differences between companies are usually price, rate history, household discounts, underwriting practices, customer service, and financial strength, not whether one company’s Plan G pays more Medicare-approved benefits than another company’s Plan G.

Finding 4: Medicare Advantage Can Be Cost-Effective, But the Tradeoffs Are Real

Medicare Advantage is not automatically bad, and it is not automatically the best choice. It is a different structure.

Medicare Advantage plans are offered by private insurance companies approved by Medicare. They replace how you receive Part A and Part B services for the year you are enrolled. Many plans include prescription drug coverage and extra benefits such as dental, vision, hearing, transportation, fitness benefits, or over-the-counter allowances.

The appeal is obvious: many Medicare Advantage plans have low or even $0 additional premiums beyond the Part B premium. For someone who is comfortable with the plan’s provider network and local service area, this can be a reasonable choice.

The tradeoff is that costs are less predictable at the point of care. Medicare Advantage plans typically have copays, coinsurance, prior authorization rules, provider networks, service-area limitations, and an annual maximum out-of-pocket limit. That out-of-pocket limit is valuable protection, but it is not the same as having low out-of-pocket costs. It is the ceiling on covered in-network medical cost-sharing, not a guarantee that care will be cheap or easy to access.

For a direct comparison of the two structures, see Medigap vs. Medicare Advantage.

Finding 5: Prior Authorization Is a Cost Factor, Not Just an Administrative Issue

Prior authorization is often described as paperwork, but for the beneficiary it can also become a cost and access issue. If a service requires approval before it is covered, the practical cost of care includes delay, uncertainty, provider administrative burden, and the possibility of appeal.

KFF has reported that Medicare Advantage insurers made tens of millions of prior authorization determinations in recent years, with millions of requests fully or partially denied. Some denials are eventually overturned on appeal, but many beneficiaries never appeal.

This does not mean a Medicare Advantage plan should never be chosen. It does mean that a fair cost comparison should include more than premiums and copays. A person who expects frequent specialist care, advanced imaging, outpatient procedures, or ongoing therapy should ask how the plan handles referrals, prior authorization, and network access before enrolling.

Finding 6: Drug Coverage Can Change the Winner

Prescription drug coverage is one of the most common places people make a Medicare mistake. Two people can choose the same medical coverage and still have very different total costs because their medications are different.

With Original Medicare and Medigap, prescription drug coverage is usually handled through a separate Part D plan. With many Medicare Advantage plans, drug coverage is included through an MA-PD plan. Either way, the details matter: premium, deductible, formulary, pharmacy network, tier placement, prior authorization, quantity limits, and mail-order pricing.

Drug coverage should be checked every year. A plan that was excellent this year may be mediocre next year if the formulary changes. A drug that was preferred at one pharmacy may price differently at another. And a new prescription can change the best plan quickly.

For more on prescription planning, see our Medicare Part D guide.

Three Medicare Cost Profiles We See Most Often

Profile 1: The predictable-cost planner

This person is not necessarily trying to buy the cheapest Medicare setup. They are trying to reduce uncertainty. For many people in this group, the ability to use any Medicare-accepting doctor nationally is part of the value.

- Usually compares Original Medicare with Medigap Plan G or Plan N.

- Values broad provider access and fewer surprise medical bills.

- Often travels or wants access to doctors in multiple states.

- Usually accepts a higher monthly premium in exchange for lower uncertainty.

Profile 2: The low-premium local-care user

This person may reasonably choose Medicare Advantage if the plan’s network, drugs, doctors, and out-of-pocket limits fit their situation. The key is to compare the entire plan, not just the premium.

- May be comfortable with a Medicare Advantage HMO or PPO.

- Has doctors and hospitals that participate in the plan network.

- Likes extra benefits such as dental, vision, hearing, transportation, or fitness benefits.

- Accepts that copays, prior authorization, and annual plan changes are part of the structure.

Profile 3: The prescription-sensitive enrollee

This person needs a drug-first review. Medical coverage matters, but prescription pricing can dominate the annual cost calculation.

- Must compare Part D or MA-PD options carefully every year.

- May find that medication costs matter more than the medical premium difference.

- Should check preferred pharmacies, tiers, restrictions, and annual drug cost estimates.

- Should not choose a plan based only on a friend’s recommendation or a TV commercial.

What Medicare Usually Does Not Cover

Another reason premium-only comparisons fall short is that Medicare does not cover every health-related expense. Original Medicare generally does not cover most routine dental care, most routine vision care, hearing aids, long-term custodial care, cosmetic surgery, most care outside the United States, and many alternative services.

Some Medicare Advantage plans include limited dental, vision, and hearing benefits. Those extras can be valuable, but they should be evaluated carefully. A dental allowance is not the same as unlimited dental coverage. A vision benefit may help with glasses but not necessarily with every eye-care expense. Hearing benefits may depend on approved providers or devices.

Medigap usually does not add dental, vision, or hearing benefits, but it can reduce Medicare-approved medical cost exposure. This is why the comparison is not simple. Medicare Advantage often bundles more extras. Medigap often provides broader medical access and predictability. The right answer depends on which type of protection matters most to the person.

Why the First Medicare Choices Matter More Than People Realize

The first Medicare decision can be more important than people realize because future flexibility is not equal in every direction.

When someone first enrolls in both Part A and Part B and is age 65 or older, they generally have a Medigap open enrollment window. During that time, they can usually buy any Medigap policy sold in their state without medical underwriting. After that window, in many states, switching into Medigap later may require answering health questions and going through medical underwriting unless a special guaranteed issue right applies.

That creates a practical difference between starting with Medigap and starting with Medicare Advantage. A person who starts with Medigap may later decide to try Medicare Advantage during an enrollment period. But a person who starts with Medicare Advantage and later wants Medigap may not always be able to get the Medigap plan they want at the price they want, depending on state rules and health history.

This is not a reason to scare people away from Medicare Advantage. It is a reason to make the first decision carefully.

For more detail, see Medigap Open Enrollment, Medigap Underwriting, and Guaranteed Issue Rights.

A Practical 7-Step Comparison Framework

A person turning 65 should compare Medicare options in this order:

- Start with doctors and hospitals. Are your preferred providers available under the option you are considering?

- Check prescriptions. Which Part D or MA-PD plan gives the lowest realistic annual cost for your exact medications?

- Compare premium plus likely usage. Do not compare premium alone.

- Look at the bad-year scenario. What happens if you need surgery, cancer treatment, therapy, or multiple specialists?

- Consider travel and lifestyle. Do you spend extended time outside your home service area?

- Think about future flexibility. Would you be comfortable if switching later required underwriting?

- Review annually. Drug plans and Medicare Advantage plans can change every year.

Medigap vs. Medicare Advantage: Educational Comparison Table

| Question | Original Medicare + Medigap | Medicare Advantage |

| How do you receive Part A and Part B benefits? | Through Original Medicare, with Medigap helping pay some or all of your share of approved costs. | Through a private Medicare Advantage plan approved by Medicare. |

| Provider access | Generally any doctor or hospital nationwide that accepts Medicare. | Usually plan network-based; HMO/PPO rules vary by plan. |

| Monthly premium | Typically higher because Medigap has a separate monthly premium. | Often lower additional premium; many plans have $0 additional premium beyond Part B. |

| Out-of-pocket predictability | Often more predictable, especially with Plan G or similar coverage. | Depends on copays, coinsurance, MOOP, network, and plan rules. |

| Prescription drugs | Usually separate Part D plan. | Often included in MA-PD plans, but not always. |

| Dental, vision, hearing extras | Usually not included in Medigap. | Often included, but benefit depth and provider access vary. |

| Prior authorization | Original Medicare generally has fewer prior authorization requirements than MA for many services. | Prior authorization can be a significant part of the plan structure. |

| Switching later | Changing Medigap later may require underwriting in many states. | Can generally change MA plans during applicable enrollment periods, subject to plan availability. |

Common Mistakes This Study Is Designed to Prevent

Mistake 1: Making Medicare choices based on premium only

A low premium is helpful, but it should be weighed against copays, coinsurance, drug costs, out-of-pocket limits, provider access, and prior authorization rules.

Mistake 2: Assuming all doctors take all Medicare plans

A doctor who accepts Original Medicare may not be in every Medicare Advantage network. Provider access must be checked plan by plan.

Mistake 3: Ignoring prescriptions

Prescription coverage should never be guessed. Drug lists, pharmacies, prior authorization, and tiers can change the annual cost quickly.

Mistake 4: Believing dental, vision, and hearing extras are unlimited

Extra benefits can be useful, but they often come with limits, provider rules, annual allowances, or specific networks.

Mistake 5: Waiting too long to understand Medigap underwriting

In many states, the easiest time to buy Medigap is when first eligible. Waiting can reduce future flexibility.

Mistake 6: Thinking Medicare choices are permanent

Some choices can be reviewed annually, but not every switch is guaranteed in every direction. That is why the first decision deserves careful attention.

Download Our Cost-Planning pdf Worksheet for Personal Use

Conclusion: The Best Medicare Choice Is the One You Understand Before You Need It

The best Medicare choices are not always the one with the lowest premium. It is the one whose tradeoffs you understand before you need care.

For some people, that will mean Original Medicare with a Medigap plan and a separate Part D plan. For others, it may mean a Medicare Advantage plan that fits their doctors, prescriptions, budget, and local care patterns. The important point is that the decision should be made with a full view of cost: premium, deductible, copays, coinsurance, drug costs, network rules, prior authorization, travel, and future flexibility.

At 65Medicare.org, our goal is to help people entering Medicare make that decision calmly and clearly. Medicare is too important to choose based on a TV ad, a mailbox flyer, or a single premium number.

To continue comparing your options, start with the Turning 65 Medicare Guide, then review Medigap vs. Medicare Advantage and How to Choose the Best Medigap Plan.

External Sources Used in this Study

CMS: 2026 Medicare Parts A & B Premiums and Deductibles

Medicare.gov: 2026 Medicare Costs Fact Sheet

Medicare.gov: Compare Medigap Plan Benefits

KFF: Medicare Advantage 2026 Spotlight – Plan Premiums and Benefits

KFF: Medicare Advantage 2026 Spotlight – Plan Offerings

KFF: Medicare Advantage prior authorization determinations in 2024