Like our Turning 65 Medicare Guide? Download a pdf for printing or reading later.

Turning 65 is the point when Medicare moves from something you have heard about to something you have to act on. The problem is that Medicare decisions are not all made at one time, and the wrong sequence can create late penalties, coverage gaps, or a plan choice that is harder to change later.

This guide walks through the full process in plain English: when to enroll in Medicare, how Parts A and B work, what Medicare costs in 2026, whether you need Part D, how Medigap compares with Medicare Advantage, what to do if you are still working, and the deadlines that matter most.

The goal is not to make Medicare more complicated. The goal is to help you understand the order of decisions. First, you determine whether you need Medicare at 65. Second, you decide whether Original Medicare or Medicare Advantage is the better structure for you. Third, you add the coverage pieces you need, such as a Medigap plan and Part D prescription drug plan. Finally, you make sure everything starts on the correct date.

For a shorter printable overview, you can also use our Turning 65 Roadmap, but this guide is the full step-by-step explanation.

Quick Summary: What to Do When You Are Turning 65

- Decide whether you need Medicare at 65 or can delay because you or your spouse are still actively working and covered by qualifying employer group health insurance.

- Enroll in Medicare Part A and Part B if Medicare will be your primary coverage when you turn 65.

- Choose between Original Medicare with optional Medigap plan and Part D, or a Medicare Advantage plan.

- If choosing Original Medicare, compare Medigap plans during your one-time Medigap Open Enrollment window.

- Compare Part D prescription drug plans based on your medications, pharmacy, and zip code.

- Make sure your effective dates line up so there is no gap between employer coverage, Medicare, Medigap, Part D, or Medicare Advantage coverage.

- Keep records of your Medicare card, enrollment confirmations, plan documents, and any employer coverage forms if you delay Part B.

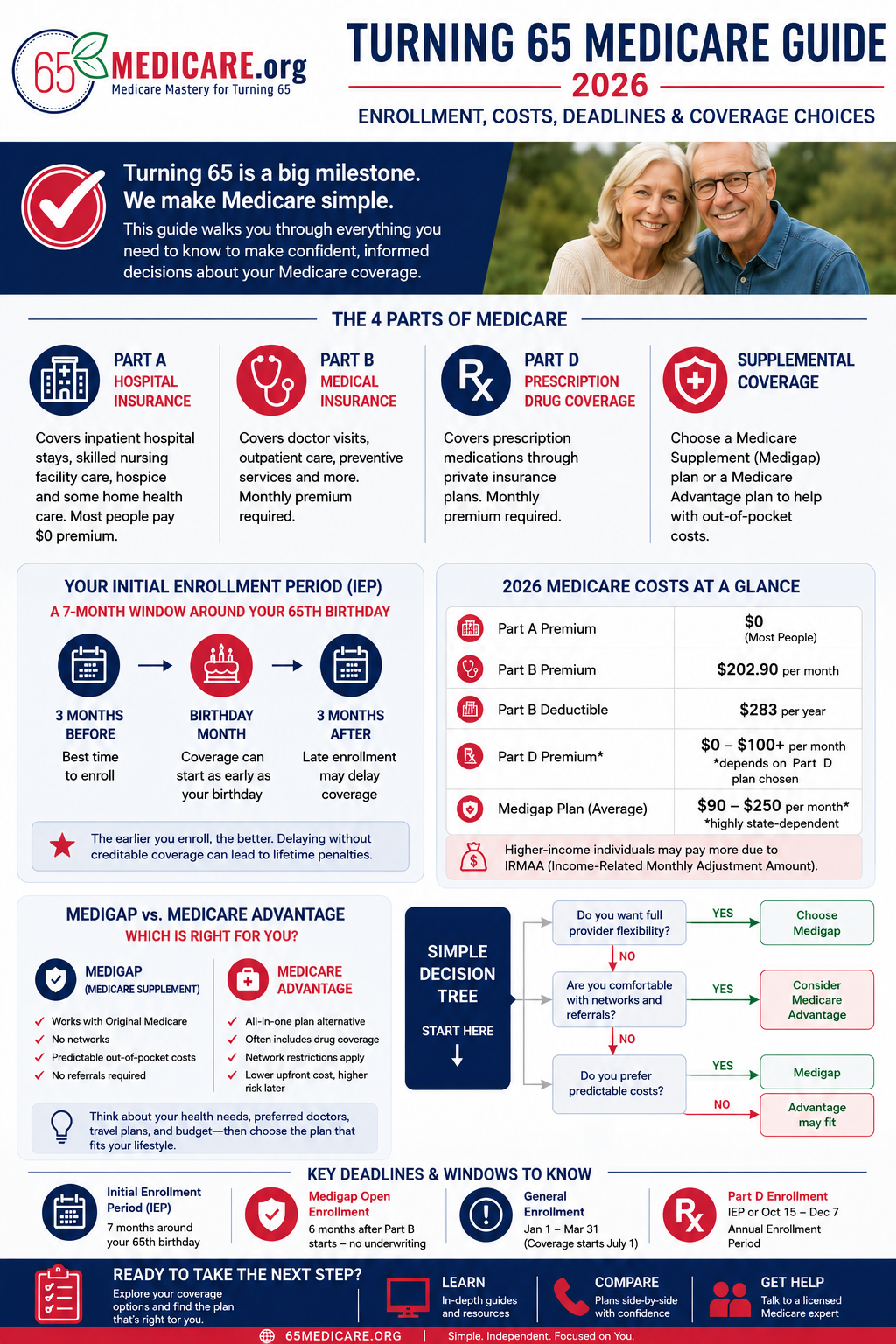

The Big Picture: Medicare Has Four Main Parts

Before you choose coverage, it helps to understand what each part of Medicare does. Medicare.gov has a helpful official overview of the parts of Medicare, but here is the practical version for someone turning 65.

| Part | What it generally covers | How it affects your decision |

| Part A | Inpatient hospital care, skilled nursing facility care after a qualifying hospital stay, hospice, and some home health care. | Most people receive Part A premium-free. If you are contributing to an HSA, enrolling in any part of Medicare can affect future HSA contributions. |

| Part B | Doctor services, outpatient care, durable medical equipment, preventive care, lab work, imaging, surgeries, chemotherapy, and many other medical services. | Part B has a monthly premium and is usually required if Medicare will be your primary coverage. Part B also starts your Medigap Open Enrollment window. |

| Part C / Medicare Advantage | A private-plan alternative to Original Medicare. You still have Medicare, but your care is managed through a private Medicare Advantage plan. | Often includes networks, copays, prior authorization rules, and usually prescription drug coverage. Plan availability depends on county. |

| Part D | Outpatient prescription drug coverage through private insurance companies approved by Medicare. | If you use Original Medicare, you usually need a stand-alone Part D plan unless you have other creditable drug coverage. |

For more detail on Part B specifically, link this section to your existing page: Medicare Part B – The Bottom Line.

Turning 65 Decision Tree: Should You Enroll in Medicare Now?

| Question | If yes | If no |

| Are you already receiving Social Security benefits before age 65? | You will usually be automatically enrolled in Part A and Part B. Review your Medicare card and decide whether to keep or decline Part B if you have qualifying employer coverage. | You generally need to actively sign up for Medicare if you want coverage to begin at 65. |

| Will you or your spouse still be actively working with employer group health coverage? | Ask the employer whether Medicare is primary or secondary and whether you can delay Part B without penalty. Employer size and plan rules matter. | You likely need Part A and Part B when you turn 65 if Medicare will be your primary coverage. |

| Do you contribute to an HSA? | Be careful. Once enrolled in Medicare, you generally cannot continue making HSA contributions. Discuss timing with your tax advisor or benefits department. | HSA contribution timing is less likely to affect your Medicare enrollment decision. |

| Do you have COBRA, retiree coverage, VA coverage, or an individual Marketplace plan? | Do not assume this lets you delay Part B penalty-free. These are not the same as active employer group coverage. | If you have no other coverage, enroll during your Initial Enrollment Period. |

| Do you want the broadest provider flexibility with predictable medical costs? | Original Medicare plus a Medigap plan and Part D may be the better structure to evaluate. | A Medicare Advantage plan may still be worth comparing if you are comfortable with networks and plan rules. |

Medicare Enrollment Timeline When Turning 65

Your first Medicare enrollment opportunity is called your Initial Enrollment Period. Medicare.gov explains that this period usually lasts seven months: it starts three months before the month you turn 65, includes your birthday month, and ends three months after your birthday month. Official Medicare enrollment timing.

| Timing | What to do | Why it matters |

| 6-12 months before 65 | Start learning the basics, review employer coverage if applicable, and decide whether Medicare will be primary. | This prevents a rushed decision and gives you time to compare Medigap and Medicare Advantage options. |

| 3 months before your 65th birthday month | This is usually the best time to sign up for Medicare if you need it at 65. | Enrolling early helps make sure your Medicare card arrives and coverage starts on time. |

| Your birthday month | You can still enroll, but timing can affect when coverage begins. | Waiting until this month can create unnecessary stress if you also need Medigap or Part D. |

| 1-3 months after your birthday month | You may still be inside your Initial Enrollment Period. | Coverage may start later, and you may have a gap if your prior coverage already ended. |

| After your Initial Enrollment Period | You may need a General Enrollment Period or Special Enrollment Period depending on your situation. | Late enrollment can create penalties or delays unless you had qualifying employer coverage. |

Will You Be Automatically Enrolled in Medicare?

Some people are enrolled in Medicare automatically; others have to sign up. The distinction usually depends on whether you are already receiving Social Security retirement benefits before you turn 65.

If you are already receiving Social Security benefits, you will usually be automatically enrolled in Medicare Part A and Part B. Your Medicare card normally arrives before your Medicare start date. If you want Medicare at 65, this is simple. If you have qualifying employer coverage and want to delay Part B, you need to pay attention to the instructions that come with your Medicare card.

If you are not already receiving Social Security benefits, you usually need to actively enroll in Medicare. You can apply online through Social Security, by phone, or through a local Social Security office.

For the actual step-by-step enrollment process, see How Do I Sign Up for Medicare?, which explains how to apply and what to expect after you submit your Medicare enrollment.

What Medicare Costs in 2026

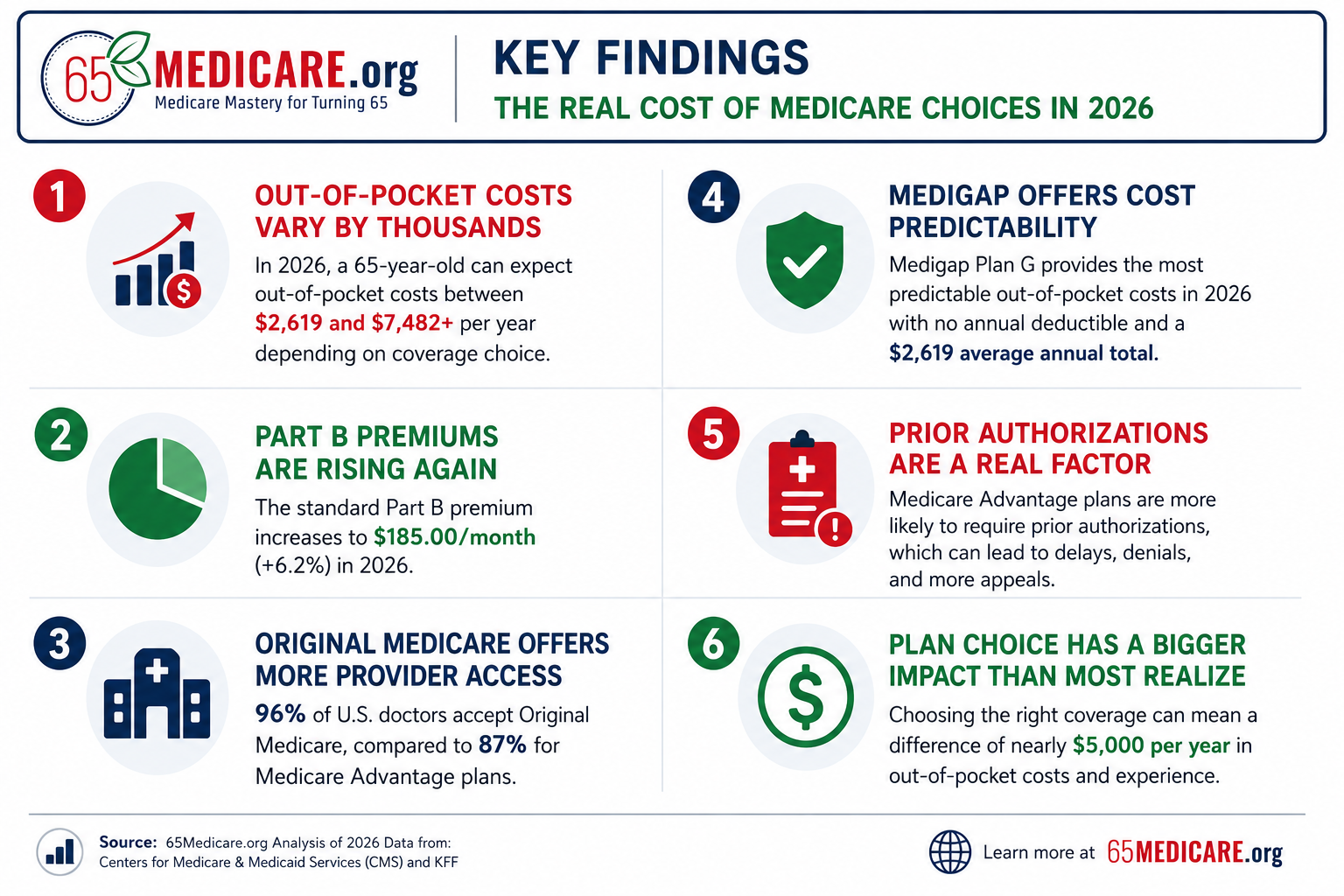

Medicare is not free. Most people receive Part A without a monthly premium, but Part B has a monthly premium, and there are deductibles, coinsurance, drug plan premiums, and optional supplemental coverage premiums to consider. CMS announced that the standard 2026 Part B premium is $202.90 per month and the 2026 Part B deductible is $283. CMS 2026 Part B premium and deductible announcement.

| Cost item | 2026 amount / range | Notes |

| Part A monthly premium | $0 for most people | Most people qualify for premium-free Part A based on work history. People without enough work credits may pay a premium. |

| Part A hospital deductible | $1,736 per benefit period | This is not an annual deductible. It can apply more than once in a year if separate benefit periods occur. |

| Part B standard monthly premium | $202.90/month | Higher-income beneficiaries may pay IRMAA in addition to the standard premium. |

| Part B annual deductible | $283/year | After the deductible, Original Medicare generally pays 80% of approved Part B charges and you pay 20%, unless you have supplemental coverage. |

| Part D premium | Varies by plan and state | Stand-alone drug plan premiums vary, and the cheapest premium is not always the best plan for your medications. |

| Part D maximum deductible | $615 in 2026 | Some plans have lower deductibles or no deductible. |

| Part D out-of-pocket cap | $2,100 in 2026 for covered Part D drugs | After reaching the cap, you pay $0 for covered Part D drugs for the rest of the year. |

| Medigap premium | Varies by age, zip code, tobacco status, household discounts, carrier, and plan letter (i.e Plan G or Plan N) | Medigap can reduce exposure to Original Medicare deductibles and coinsurance. |

| Medicare Advantage premium | Varies by county and plan | Many plans have low premiums, but you must evaluate networks, copays, maximum out-of-pocket limits, drug coverage, and prior authorization rules. |

For detailed Part B cost discussion, link to: What Does Medicare Part B Cost? For Part D cost structure, link to Medicare.gov’s official page on Medicare drug coverage costs.

IRMAA: Why Higher-Income Retirees May Pay More for Medicare

IRMAA stands for Income-Related Monthly Adjustment Amount. It is an additional amount charged to some higher-income Medicare beneficiaries for Part B and Part D. It is not based on your current income in most cases. Social Security generally uses your tax return from two years prior to determine whether IRMAA applies.

For 2026 Medicare premiums, the income being evaluated is generally 2024 modified adjusted gross income. That can surprise new retirees because the tax return used may reflect their final high-income working year, a business sale, capital gains, Roth conversions, bonuses, or other income that may not represent their current retirement income.

IRMAA can often be appealed if your income has gone down because of a qualifying life-changing event, such as retirement, reduction in work, marriage, divorce, death of a spouse, or loss of pension income. It is worth understanding before turning 65, especially if you are retiring from a high-income year.

If your income may trigger higher Medicare premiums, review What is IRMAA? and this step-by-step guide on how to appeal IRMAA after a qualifying income change.

Your Two Main Coverage Paths at 65

Once you have Medicare Part A and Part B, the biggest decision is how you want your coverage structured. Many people turning 65 begin by comparing Medigap plans versus Medicare Advantage options.

Most people choose one of two paths: Original Medicare with a Medigap plan and Part D, or Medicare Advantage.

| Coverage path | How it works | Best fit for people who… | Watch-outs |

| Original Medicare + Medigap + Part D | Medicare remains primary. A Medigap plan helps pay some or most of the deductibles and coinsurance left by Original Medicare. A stand-alone Part D plan covers prescriptions. | Want broad access to doctors nationwide, predictable medical costs, and fewer network concerns. | Usually has a separate Medigap premium and Part D premium. Does not typically include routine dental, vision, or hearing benefits. |

| Medicare Advantage | A private Medicare Advantage plan administers your Medicare benefits. Plans often include drug coverage and may include extra benefits. | Are comfortable with networks, copays, plan rules, and county-specific plan availability. | Provider networks, prior authorization, copays, annual plan changes, and maximum out-of-pocket limits matter. Moving or doctor changes can affect fit. |

For a deeper comparison of the two coverage structures, read Medigap and Medicare Advantage – How Do They Differ?, which explains the practical trade-offs between provider flexibility, networks, premiums, and out-of-pocket risk.

See our Medicare costs study (2026), which may help differentiate between these two plan types (excerpt below).

If You Choose Original Medicare: How Medigap Fits In

Original Medicare is accepted by a large number of providers across the country, but it does not have a built-in annual out-of-pocket maximum for Part A and Part B services. That is the main reason many people add a Medicare Supplement plan, also called Medigap.

Medigap plans are standardized by plan letter in most states. That means Plan G benefits are the same from one company to another, even though premiums, rate stability, household discounts, underwriting rules, and customer service can vary by company. Medigap Plan N benefits are standardized as well according to the Medigap coverage chart.

Your best time to buy a Medigap plan is usually your Medigap Open Enrollment period. This is a six-month window that starts when you are both age 65 or older and enrolled in Medicare Part B. During this window, you can buy any Medigap plan available to you without medical underwriting. In most states, waiting until later can mean you have to answer health questions and can be declined.

| Medigap issue | What to know when turning 65 |

| Plan choice | Plan G and Plan N are two of the most commonly compared options for new Medicare beneficiaries. |

| Carrier choice | Since benefits are standardized, company selection should focus on premium, rate history, household discount, underwriting posture, and financial stability. |

| Enrollment window | Your one-time Medigap Open Enrollment window is extremely important. It is not the same as the annual Medicare Open Enrollment period. |

| Prescription drugs | Modern Medigap plans do not include Part D drug coverage. If you choose Original Medicare plus Medigap, you usually need a separate Part D plan. |

| Networks | Medigap plans do not have HMO or PPO networks. If a provider accepts Medicare, the Medigap plan generally works with Medicare-approved services. |

To compare the major Medicare Supplement options, start with our Medigap Plans (2026 Guide), then review when Medicare Supplement Open Enrollment begins and use the Medigap Coverage Chart to see what each standardized plan letter covers.

Prescription Drug Coverage: Why Part D Still Matters

Original Medicare does not cover most outpatient prescription drugs. If you choose Original Medicare, you generally need a stand-alone Part D plan unless you have other creditable drug coverage. Even people who take few or no medications often choose a low-cost Part D plan to avoid future late enrollment penalties and to protect against unexpected prescriptions.

Part D plans are not one-size-fits-all. The best plan depends on your medications, pharmacy, zip code, deductible, copays, coinsurance, formulary, and whether your prescriptions are covered at preferred pharmacies.

For 2026, Medicare.gov states that no Medicare drug plan may have a deductible greater than $615, and the out-of-pocket cap for covered Part D drugs is $2,100. That cap is helpful, but it does not mean every medication is covered. You still have to compare plan formularies carefully.

| Part D decision | Practical guidance |

| I take no prescriptions | You may still want a low-cost plan to avoid a late enrollment penalty and preserve coverage if medications change. |

| I take several medications | Run a plan comparison using exact drug names, dosages, quantities, and pharmacy preferences. |

| I take expensive medications | Look closely at formulary coverage, prior authorization, step therapy, preferred pharmacies, and the 2026 out-of-pocket cap. |

| I have VA drug coverage | VA coverage may be creditable, but coordinate carefully before skipping Part D. |

| I am choosing Medicare Advantage | Many Medicare Advantage plans include drug coverage, but not all do. Make sure drug coverage is included if you need it. |

Because drug plan fit depends on your medications and pharmacy, use our step-by-step guide to comparing Part D plans and review whether you have to sign up for a Medicare Part D plan when you first become eligible.

What If You Are Still Working at 65?

This is one of the most important sections for people turning 65. If you or your spouse are still actively working and you have employer group health coverage, you may be able to delay Medicare Part B without penalty. But you should not guess. The employer size, plan rules, whether coverage is based on current employment, and whether you contribute to an HSA all matter.

In general, active employer coverage can create a Special Enrollment Period later. COBRA, retiree coverage, VA coverage, and Marketplace coverage are different and should not be treated the same as active employer group coverage for Part B timing purposes.

If you delay Part B because you are covered by active employment, keep records. When you later enroll in Part B, Social Security may require employer verification showing that you had qualifying group health coverage after age 65.

| Coverage situation at 65 | Can you usually delay Part B penalty-free? | Key caution |

| Active employer group coverage through your or your spouse’s current job | Often yes, but confirm with the employer and insurer. | Employer size and plan coordination rules matter. |

| COBRA | Usually no for delaying Part B after 65. | COBRA can create serious gaps or penalties if treated like active employer coverage. |

| Retiree coverage | Usually no for delaying Part B penalty-free. | Retiree coverage often expects Medicare to be primary. |

| Marketplace/ACA individual plan | Usually no. | You may lose premium tax credits when eligible for premium-free Part A. |

| VA coverage | VA drug coverage can be valuable, but it is not the same as Medicare Part B coverage. | VA and Medicare work in different systems; many veterans enroll in Part B. |

| TRICARE for Life | You generally need Part A and Part B. | Failing to enroll in Part B can affect TRICARE eligibility. |

If you or your spouse will keep working after 65, read our Working Past 65: Medicare Special Enrollment Guide before deciding whether to delay Part B.

Medicare Late Enrollment Penalties to Avoid

Medicare penalties are frustrating because they are often permanent or long-lasting. The most common penalties involve Part B and Part D.

The Part B late enrollment penalty can apply if you did not sign up for Part B when first eligible and did not have qualifying coverage that allowed you to delay. The penalty is generally based on how long you went without Part B after you should have had it.

The Part D late enrollment penalty can apply if you go without Part D or other creditable prescription drug coverage for too long after your initial eligibility. Even if you are healthy, this is one reason many people choose a low-premium Part D plan when they first start Medicare.

| Penalty risk | How to avoid it |

| Part B late enrollment penalty | Enroll during your Initial Enrollment Period unless you have qualifying active employer group coverage that allows you to delay. |

| Part D late enrollment penalty | Enroll in a Part D plan when first eligible unless you have other creditable drug coverage. |

| Coverage gap | Enroll early enough so Medicare and any supplemental coverage begin when prior coverage ends. |

| Missed Medigap Open Enrollment | Use your six-month Medigap window wisely if you want a Medigap plan without underwriting. |

For a deeper explanation of how penalties work, see Medicare Late Enrollment Penalties: The Importance of Enrolling on Time.

90-Day Turning 65 Medicare Checklist

| When | Action step |

| 6-12 months before 65 | Learn the difference between Original Medicare, Medigap, Medicare Advantage, and Part D. Review your employer coverage if you are still working. |

| 4-6 months before 65 | Decide whether Medicare will be primary at 65. If still working, ask HR whether you can delay Part B and whether Medicare affects HSA eligibility. |

| 3 months before 65 | Apply for Medicare Part A and Part B if you need Medicare at 65. This is usually the best time to apply. |

| 2-3 months before coverage begins | Compare Medigap plans and/or Medicare Advantage plans. Compare Part D plans using your actual prescriptions. |

| 1 month before coverage begins | Confirm your Medicare card, plan approvals, effective dates, premiums, and prescription plan details. |

| After coverage begins | Create a Medicare.gov account, keep plan documents, verify your doctors and pharmacies, and review Part D annually. |

Common Turning 65 Medicare Mistakes

| Mistake | Why it matters | Better approach |

| Assuming Medicare is automatic for everyone | Many people must actively sign up. | Confirm whether you are receiving Social Security and whether you need to apply. |

| Confusing Medigap Open Enrollment with annual Medicare Open Enrollment | Annual Open Enrollment is mainly for Part D and Medicare Advantage changes, not guaranteed Medigap enrollment. | Understand your one-time six-month Medigap window. |

| Choosing a plan based only on premium | Low premium can come with network limits, copays, or higher risk of future out-of-pocket costs. | Compare total cost, access, flexibility, and risk. |

| Skipping Part D because you take no medications | You may face a penalty later and could be uncovered if prescriptions change. | Consider a low-cost Part D plan unless you have creditable drug coverage. |

| Relying on COBRA to delay Part B | COBRA is not the same as active employer coverage. | Get Medicare timing advice before using COBRA after age 65. |

| Ignoring IRMAA | Higher-income retirees may be surprised by additional Part B and Part D premiums. | Review MAGI, retirement timing, and appeal options if income has dropped. |

You can also review these five crucial Medicare mistakes people make when turning 65 so you avoid the most common errors before your coverage begins.

Coverage Start Dates and Special Birthday Rules

Most people want Medicare to begin the first day of the month they turn 65. That is usually possible when you enroll during the three months before your birthday month. If you wait until your birthday month or later in your Initial Enrollment Period, your coverage start date can be delayed.

There is also a special timing rule for people born on the first day of a month. If your birthday is on the first day of the month, Medicare eligibility generally begins on the first day of the previous month. That can affect when you should apply, when Part B begins, and when your Medigap Open Enrollment window starts.

This is one reason it is best not to wait until the last minute. Medicare, Medigap, Part D, employer coverage termination dates, and Social Security billing can all interact. A one-month timing mistake can cause either a gap in coverage or duplicate premiums.

| Situation | Likely timing issue | Recommended action |

| Birthday is not on the 1st of the month | Medicare usually starts the first day of your birthday month if you enroll early. | Apply during the three months before your birthday month. |

| Birthday is on the 1st of the month | Medicare eligibility generally starts the first day of the prior month. | Start planning one month earlier than you otherwise would. |

| Retiring after 65 | Your Part B date may be based on loss of active employer coverage rather than your birthday. | Coordinate employer forms, Part B start date, Medigap, and Part D. |

| Employer coverage ends at month-end | You need Medicare and related coverage to begin the next day. | Do not rely on COBRA unless you have confirmed the Medicare consequences. |

How to Sign Up for Medicare: Practical Step-by-Step

Medicare enrollment itself is handled through Social Security, not through an insurance company. Insurance companies and brokers can help you with Medigap, Part D, and Medicare Advantage choices, but Medicare Part A and Part B enrollment generally goes through Social Security.

The online application is usually the easiest method for people who are not already receiving Social Security. If you prefer, you can also call Social Security or make an appointment with a local Social Security office. The important point is to apply early enough that your Medicare card arrives before you need to enroll in any additional coverage.

- Create or log in to your Social Security account.

- Choose the Medicare-only enrollment path if you want Medicare but do not want to start Social Security retirement benefits yet.

- Select the desired start date for Part B if the application asks for it and your situation allows a choice.

- Watch for confirmation and your red, white, and blue Medicare card.

- Review the effective dates on the card before applying for Medigap, Part D, or Medicare Advantage.

- Keep copies of confirmations, employer forms, and plan approvals.

Official external link: Social Security – Sign up for Medicare.

What Original Medicare Does Not Fully Cover

A common mistake is assuming Medicare works like a traditional employer health plan. Original Medicare is strong coverage, but it does not cover everything and it does not automatically include a cap on your annual medical spending for Part A and Part B services.

This does not mean Original Medicare is poor coverage. It means you need to understand the gaps and decide whether to fill them with Medigap, Part D, dental/vision/hearing coverage, or another strategy.

| Gap or limitation | Why it matters |

| No built-in annual out-of-pocket maximum for Original Medicare Part A and Part B | Without Medigap or other coverage, repeated hospitalizations, surgeries, chemotherapy, or outpatient services can create significant cost exposure. |

| Most outpatient prescriptions are not covered by Original Medicare | You usually need Part D or other creditable drug coverage. |

| Routine dental, vision, and hearing are limited or not covered in many situations | Some people buy separate coverage or choose Medicare Advantage partly for these benefits. |

| Long-term custodial care is not covered | Medicare may cover limited skilled care, but not ongoing custodial nursing home or assisted living care. |

| Foreign travel coverage is limited | Some Medigap plans include limited foreign travel emergency coverage; Original Medicare generally does not cover routine foreign care. |

| Provider billing rules still matter | Doctors who accept assignment, excess charges, and Medicare-approved amounts can affect your out-of-pocket costs. |

Sample Coverage Setups for Common Turning 65 Situations

| Scenario | Likely coverage setup to evaluate | Why |

| Retiring at 65 with no employer coverage continuing | Part A + Part B, then compare Original Medicare + Medigap + Part D vs Medicare Advantage. | Medicare will likely become primary, so the full coverage structure matters immediately. |

| Still working with strong employer coverage through a large employer | Possibly delay Part B; possibly enroll in Part A only; evaluate HSA impact. | Employer coverage may allow delayed Part B, but HSA and coordination rules must be confirmed. |

| High income in final working years | Part A/Part B timing plus IRMAA review and possible appeal if retirement lowers income. | IRMAA may be based on an older high-income tax return. |

| Takes multiple prescriptions | Part D comparison based on drug list, dosage, pharmacy, formulary, and 2026 cost cap. | Premium alone is not enough to choose a Part D plan. |

| Travels frequently or spends time in multiple states | Original Medicare + Medigap + Part D may deserve strong consideration. | Provider flexibility and lack of networks can matter more for frequent travelers. |

| Has a tight monthly budget and uses local doctors | Medicare Advantage may be worth comparing carefully. | Lower premiums may be attractive, but networks, copays, and maximum out-of-pocket exposure must be reviewed. |

How to Compare Medicare Options Without Getting Overwhelmed

The biggest mistake is trying to compare every advertisement, every mailer, every TV commercial, and every plan at the same time. Instead, compare Medicare options in layers.

Start with structure: Do you want Original Medicare or Medicare Advantage? Then compare the specific plan type. If you choose Original Medicare, compare Medigap plan letters first, then insurance companies, then Part D. If you choose Medicare Advantage, compare networks, drugs, copays, maximum out-of-pocket limits, star ratings, and plan stability.

| Comparison layer | Questions to ask |

| Coverage structure | Do I want Original Medicare with optional Medigap and Part D, or do I want Medicare Advantage? |

| Doctors and hospitals | Are my doctors accessible? Do I need referrals? Am I limited to a network? |

| Prescription drugs | Are my drugs covered? Are there restrictions? Which pharmacies are preferred? |

| Total cost risk | What are the premium, deductible, copays, coinsurance, and worst-case annual exposure? |

| Travel and flexibility | Will this work if I travel, move, snowbird, or want to see specialists in another area? |

| Future changes | How easy is it to change later if my health, medications, doctors, or budget changes? |

What Happens After You Enroll: Annual Reviews and Ongoing Decisions

Medicare is not a one-time decision that you never revisit. Some parts of your coverage should be reviewed annually, while other parts may remain stable for years.

Part D plans should be reviewed regularly because formularies, premiums, deductibles, preferred pharmacies, and drug tiers can change every year. Medicare Advantage plans should also be reviewed annually because benefits, networks, copays, maximum out-of-pocket limits, and service areas can change. Medigap plans are different: they are guaranteed renewable, and you generally do not have to re-enroll each year. However, premiums can increase, and changing Medigap plans later may require underwriting in most states.

| Coverage type | Review frequency | Reason |

| Original Medicare Part A and Part B | Ongoing, but benefits are federal and generally stable | Costs and deductibles can change annually. |

| Medigap | Review premiums periodically | Benefits are standardized, but premiums and carrier competitiveness can change. |

| Part D | Review every year | Drug formularies, premiums, pharmacy networks, and copays change frequently. |

| Medicare Advantage | Review every year | Networks, benefits, service areas, copays, and drug coverage can change annually. |

| IRMAA | Review when income changes | Retirement, reduced work, or other life-changing events may create appeal opportunities. |

How 65Medicare.org Helps People Turning 65

Medicare is easier when the decisions are made in the right order. At 65Medicare.org, we help people turning 65 understand when to enroll, how to compare Medigap and Medicare Advantage, how Part D fits in, and how to avoid common mistakes that can be hard to unwind later.

We are an independent Medicare insurance agency. That means we can help you compare options from multiple companies rather than forcing you into one company’s plan. If you want Medigap quotes by email, help comparing plans, or a phone appointment to walk through your situation, you can start below.

Get Medigap quotes by email: https://65medicare.org/medigap-quotes-email/

Schedule a phone appointment: https://calendly.com/garrettball

Like our Turning 65 Medicare Guide? Download a pdf for printing or reading later.

FAQ: Turning 65 and Medicare

When should I sign up for Medicare if I am turning 65?

If Medicare will be your primary coverage at 65, the best time is usually during the three months before your 65th birthday month. Your Initial Enrollment Period lasts seven months total, but applying early helps reduce the risk of delays.

Do I have to sign up for Medicare at 65 if I am still working?

Not always. If you or your spouse are actively working and covered by qualifying employer group health insurance, you may be able to delay Part B without penalty. However, you should confirm this with the employer and understand HSA, COBRA, retiree coverage, and employer-size rules.

Is Medicare free when you turn 65?

No. Most people receive Part A premium-free, but Part B has a monthly premium. In 2026, the standard Part B premium is $202.90 per month, and higher-income beneficiaries may pay more because of IRMAA.

What is the difference between Medicare and Medigap?

Medicare is the federal health insurance program. Medigap is private supplemental insurance that helps pay some of the deductibles and coinsurance left behind by Original Medicare.

Do I need a Part D plan if I do not take prescriptions?

Many people still enroll in a low-cost Part D plan to avoid future late enrollment penalties and to protect themselves if medication needs change. You may not need Part D if you have other creditable drug coverage.

Is Medicare Advantage the same as Medigap?

No. Medicare Advantage is an alternative way to receive Medicare benefits through a private plan. Medigap works with Original Medicare and helps pay Original Medicare cost-sharing. You cannot use Medigap to pay Medicare Advantage copays.

Can I switch from Medicare Advantage to Medigap later?

You may be able to apply, but in most states you may have to answer health questions outside your Medigap Open Enrollment or guaranteed issue window. This is one reason the first-year decision is important.

What happens if I miss my Initial Enrollment Period?

You may have to wait for another enrollment period, and you may face late enrollment penalties unless you qualify for a Special Enrollment Period based on qualifying coverage.

What is the most important Medicare deadline when turning 65?

There are several, but the most important are your Initial Enrollment Period for Medicare Parts A and B, your Part D enrollment timing, and your six-month Medigap Open Enrollment window if you want a Medicare Supplement plan.

Does the annual Medicare Open Enrollment period apply to Medigap?

Not in the way many people think. The annual October 15 to December 7 period is mainly for Medicare Advantage and Part D changes. It does not create a nationwide annual guaranteed-issue Medigap enrollment period.