Medigap plans, also called Medicare Supplement plans, are private insurance policies that work with Original Medicare to help pay some of the costs Medicare leaves behind. Those costs can include deductibles, coinsurance, copayments, and in some cases excess charges or foreign travel emergency care. If you are turning 65, losing employer coverage, moving away from Medicare Advantage, or simply trying to lower your long-term out-of-pocket risk, understanding Medigap is one of the most important Medicare decisions you will make.

Start here: Medigap plans are standardized. A Plan G from one insurance company provides the same medical benefits as a Plan G from another insurance company. The difference is not the claims process or whether one company “covers more.” The real differences are price, rate history, underwriting rules, discounts, household eligibility, and how each company is positioned in your state.

Use this guide as the main starting point for comparing Medigap plans in 2026. We will cover how Medigap works, which plans are most commonly chosen, how Plan G compares with Plan N and High-Deductible Plan G, how state rules can change the equation, when underwriting applies, what to watch for with rate increases, and how to choose a plan that fits your actual situation.

Want the Short Version?

If you already understand Medicare and want to compare rates, the next practical step is to get a list of Medigap rates and company ratings for your specific ZIP code. You can compare Medigap quotes by email through 65Medicare.org without being pushed into a plan before you understand your options.

What Are Medigap Plans?

Medigap is extra insurance sold by private insurance companies to people enrolled in Original Medicare. It is designed to help pay your share of costs under Medicare Part A and Part B. Original Medicare pays first, and the Medigap plan pays second according to the standardized benefits of the plan you choose.

Medigap does not replace Medicare. You must remain enrolled in Medicare Part A and Part B. In most cases, you also need a separate Medicare Part D prescription drug plan because modern Medigap plans do not include drug coverage. If you are unsure how drug coverage fits into this decision, review whether you have to sign up for Medicare Part D before finalizing your Medigap choice.

Most people choose a Medigap plan for three main reasons: predictable costs, freedom to use any provider that accepts Medicare, and protection from large Original Medicare cost-sharing exposure. Original Medicare does not have an annual out-of-pocket maximum. That means someone who uses only Original Medicare could be responsible for repeated deductibles and 20% coinsurance on covered Part B services without a yearly cap.

| Medigap Feature | Why It Matters |

| Works with Original Medicare | Medicare remains your primary coverage; the supplement fills some or most of the gaps. |

| No provider networks | You can use any doctor or hospital that accepts Medicare, subject to Medicare rules. |

| Standardized benefits | Plan G is Plan G regardless of company; Plan N is Plan N regardless of company. |

| Separate from Part D | You usually need a separate prescription drug plan. |

| Usually no annual plan shopping required | Medigap policies are guaranteed renewable as long as premiums are paid. |

How Medigap Works With Original Medicare

When you receive covered care, the provider bills Medicare first. Medicare processes the claim and pays its approved portion. Then the claim typically crosses over electronically to your Medigap insurance company. The Medigap company pays according to your plan’s standardized benefits. In most situations, you do not file paper claims or negotiate with the insurance company.

This “crossover” process is one of the practical reasons many people prefer Medigap. If the provider accepts Medicare, the supplement is designed to coordinate behind Medicare. That is very different from a network-based plan where you may need to confirm whether a provider participates in a specific plan network.

| Coverage Type | How It Works |

| Original Medicare only | Medicare pays its share; you are responsible for deductibles and coinsurance with no annual out-of-pocket cap. |

| Original Medicare + Medigap | Medicare pays first; Medigap pays second based on the standardized plan benefits. |

| Medicare Advantage | You receive Medicare benefits through a private plan with networks, plan rules, copays, and annual changes. |

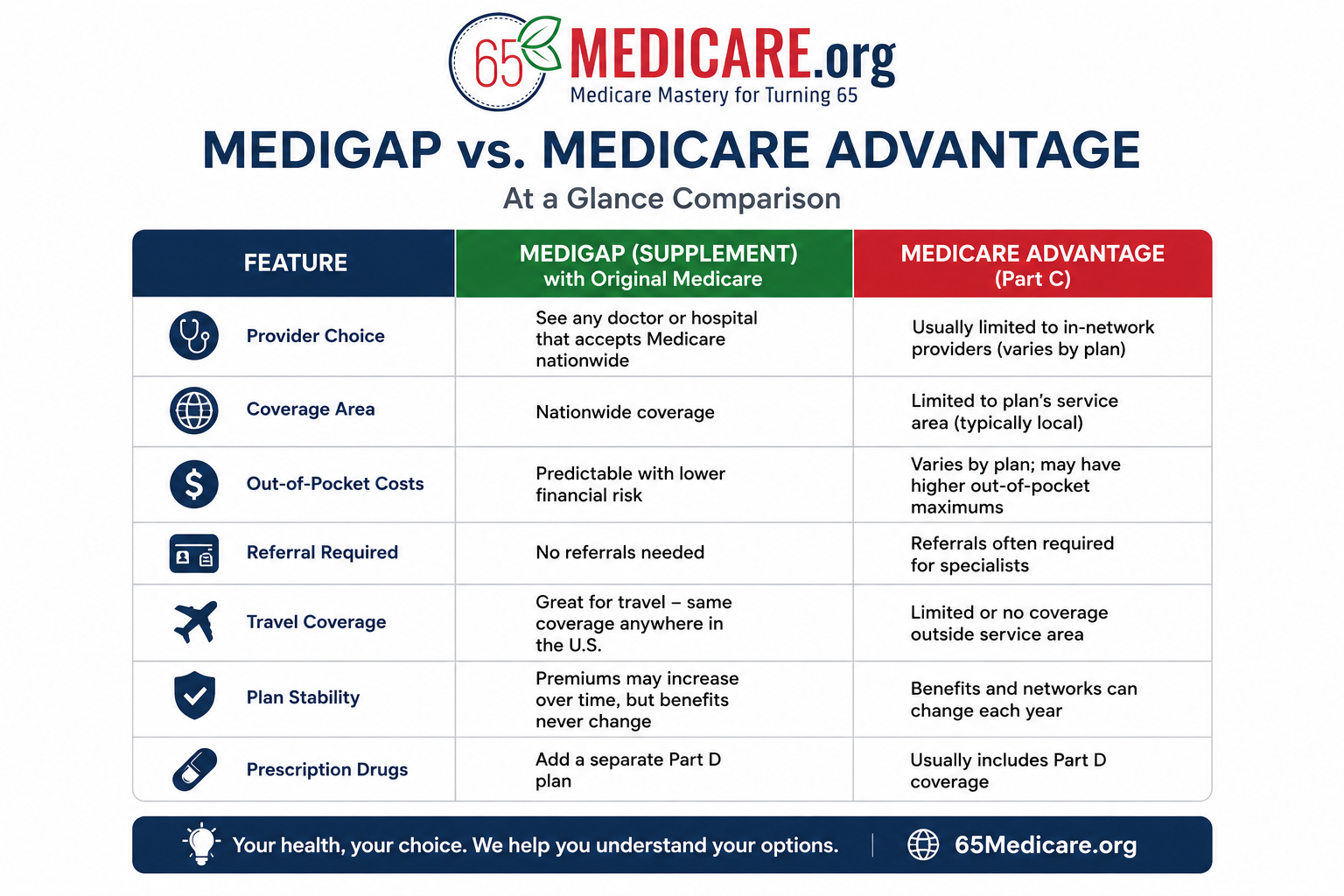

If you are comparing Original Medicare with a supplement against an all-in-one private plan, read the full comparison of Medigap vs Medicare Advantage before choosing. That decision affects provider access, referrals, prior authorization, travel flexibility, and long-term ability to change coverage.

Why Medigap Standardization Matters

Medigap standardization is the key to comparing plans correctly. In most states, Medigap plans are labeled A, B, C, D, F, G, K, L, M, and N. Each lettered plan has a set package of benefits. For example, a Plan G from Company A must provide the same standardized medical benefits as a Plan G from Company B.

That is why “which company has the best coverage?” is usually the wrong starting question. For the same plan letter, the benefits are the same. The better question is: Which company gives me the best combination of price, stability, underwriting flexibility, discounts, and long-term value in my state?

Medicare’s own comparison chart confirms that Medigap plan benefits are standardized in most states. You can compare the official benefit categories through Medicare.gov’s Medigap plan benefits chart and then use that framework to compare real premiums in your area.

| Factor | Same Across Companies? | Why It Matters |

| Benefits for the same plan letter | Yes | A Plan G is standardized, so medical benefits are the same. |

| Premium | No | Companies can charge very different rates for identical benefits. |

| Rate increase history | No | Some companies may have more stable long-term pricing than others. |

| Household discounts | No | Discounts vary by company and state. |

| Underwriting rules | No | If you switch later, company-specific underwriting matters. |

| Availability by state | No | Not every company sells every plan in every state. |

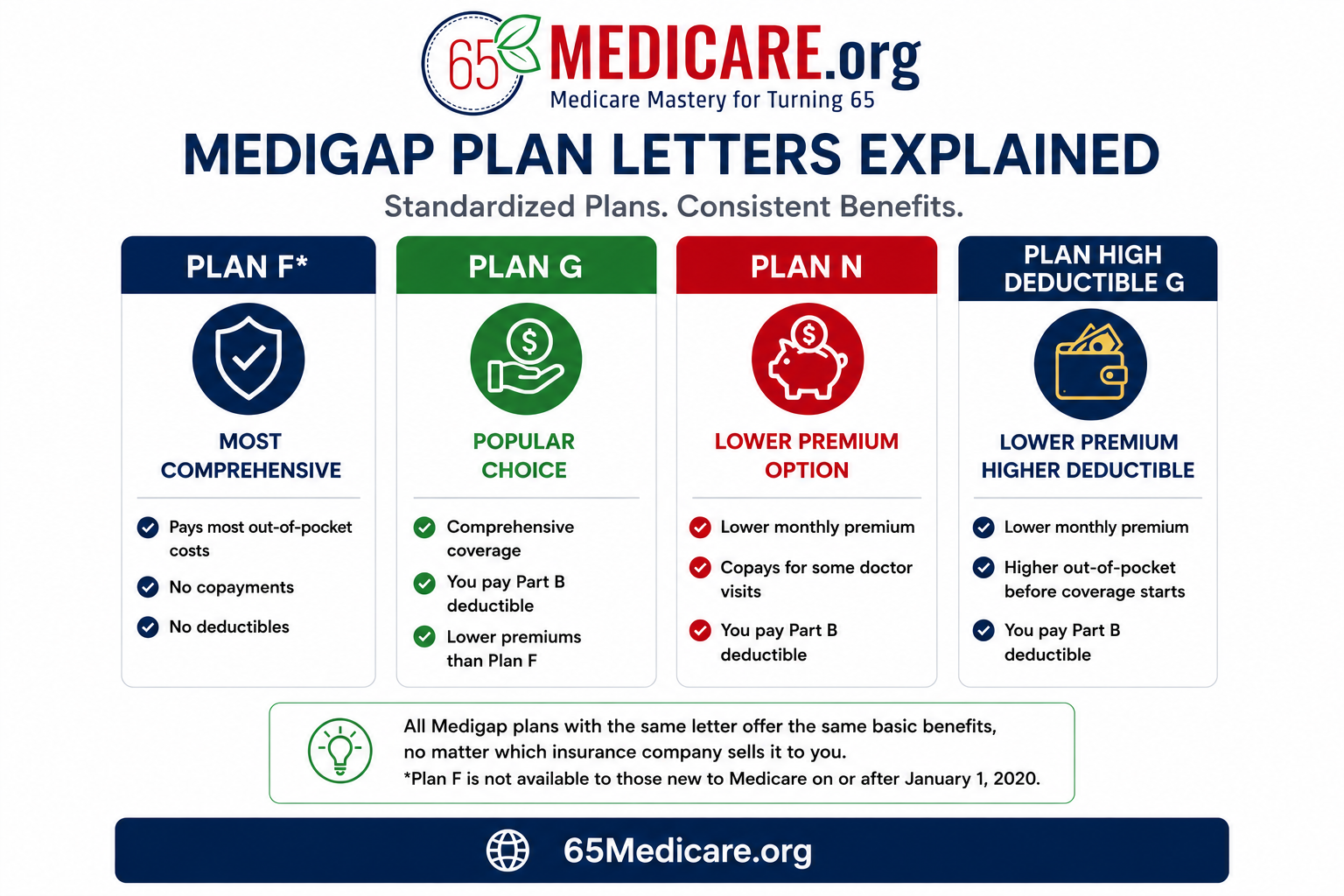

Best Medigap Plans in 2026: The Short Answer

For most people turning 65 in 2026, the practical Medigap comparison comes down to three choices: Plan G, Plan N, and High-Deductible Plan G. Other plans exist, and in some cases they can make sense, but these three usually represent the most practical decision points: maximum predictability, lower premium with some cost-sharing, or very low premium with higher out-of-pocket exposure.

| Plan | Best Fit | Main Strength | Main Tradeoff |

| Plan G | People who want predictable costs and broad protection | Covers nearly all Medicare-approved gaps after the Part B deductible | Higher monthly premium than Plan N or HDG |

| Plan N | People willing to accept some copays to reduce premium | Lower monthly premium with strong overall coverage | Copays may apply; does not cover Part B excess charges |

| High-Deductible Plan G | People who want low premium and can absorb more risk | Very low monthly premium with catastrophic-style Medigap protection | Must meet the annual high deductible before plan pays |

| Plan F | People eligible before 2020 who already have or can still buy it | Most comprehensive standardized coverage | Often higher premium and potentially less attractive long-term value |

| Plan A/B/D/K/L/M | Narrower situations or state-specific pricing opportunities | May be useful where pricing is unusually favorable | Less commonly selected and often not the best value |

Plan G is often the starting point because it is the most comprehensive plan available to people newly eligible for Medicare after January 1, 2020. Plan N is often the next comparison because it can lower the premium while keeping strong protection. High-Deductible Plan G is worth considering for people who are focused on minimizing premiums and are comfortable with a higher deductible.

Medigap Plan Comparison Chart for 2026

The following table summarizes the most common plan choices. For a full side-by-side chart of all standardized plans, use the Medigap coverage chart as a companion resource.

| Benefit / Feature | Plan G | Plan N | High-Deductible Plan G | Plan F* |

| Part A hospital coinsurance | Covered | Covered | Covered after deductible | Covered |

| Part A deductible | Covered | Covered | Covered after deductible | Covered |

| Part B coinsurance | Covered | Covered, except possible copays | Covered after deductible | Covered |

| Part B deductible | Not covered | Not covered | Not covered | Covered |

| Part B excess charges | Covered | Not covered | Covered after deductible | Covered |

| Skilled nursing facility coinsurance | Covered | Covered | Covered after deductible | Covered |

| Foreign travel emergency | 80% up to plan limits | 80% up to plan limits | 80% after deductible up to plan limits | 80% up to plan limits |

| Prescription drugs | Not included | Not included | Not included | Not included |

| Typical premium level | Higher | Moderate | Lowest | Often highest |

*Plan F is generally not available to people who became newly eligible for Medicare on or after January 1, 2020.

Medigap Plan G: Best for Predictable Costs

Medigap Plan G is usually the benchmark plan for people turning 65. It covers the major gaps in Original Medicare except for the Medicare Part B deductible. In 2026, the Part B deductible is $283. After you meet that deductible, Plan G generally covers the remaining Medicare-approved Part A and Part B cost-sharing amounts that the plan is designed to cover.

Plan G is popular because it is simple. You pay the monthly premium, you pay the annual Part B deductible when applicable, and then you generally have very little medical cost-sharing for Medicare-approved services. There are no office visit copays under Plan G, and Plan G covers Medicare Part B excess charges where they are allowed.

| Plan G Advantage | What It Means |

| High predictability | After the Part B deductible, most Medicare-approved cost-sharing is covered. |

| No Plan N-style doctor copays | You do not pay the up-to-$20 office visit copay that can apply under Plan N. |

| Covers excess charges | Useful if you see a provider who does not accept Medicare assignment in a state where excess charges are allowed. |

| Strong travel flexibility within the U.S. | No Medicare Advantage-style local network restrictions. |

| Often better value than Plan F | For many people eligible for both, Plan G premium savings can exceed the Part B deductible difference. |

Plan G is not always the cheapest option, but it is often the clearest choice for people who value low uncertainty. If you are comparing it with Plan F, the key question is whether the Plan F premium is higher by more than the Part B deductible amount. The detailed breakdown of Plan F vs Plan G explains why Plan G is frequently the better value when the premium spread is large enough.

Medigap Plan N: Best for Lower Premiums With Some Cost-Sharing

Medigap Plan N is often the most logical alternative to Plan G. It usually has a lower monthly premium than Plan G, but the tradeoff is some cost-sharing. With Plan N, you may pay up to $20 for certain office visits and up to $50 for emergency room visits that do not result in an inpatient admission. Plan N also does not cover Medicare Part B excess charges.

Plan N can make sense for someone who is relatively healthy, sees doctors infrequently, and wants to lower monthly premium cost without moving to a Medicare Advantage network-based structure. But Plan N should not be chosen only because the premium is lower. You should compare the premium savings against expected copays, provider usage, and whether excess charges are a realistic issue in your area.

| Plan N Question | Why It Matters |

| How often do you see doctors? | More visits can reduce the value of premium savings because copays may apply. |

| Do your doctors accept Medicare assignment? | Plan N does not cover Part B excess charges. |

| Is the premium difference meaningful? | A small savings may not justify giving up Plan G protections. |

| Are you comfortable with some bills? | Plan N is less predictable than Plan G but still much more structured than Original Medicare alone. |

The most common Plan G vs Plan N mistake is looking only at the monthly premium. A lower premium is attractive, but the better question is whether the savings are large enough to justify the additional variables. A healthy person with limited doctor use may find Plan N to be an excellent value. Someone who wants maximum simplicity may prefer Plan G.

High-Deductible Plan G: Best for Low Premiums and Higher Risk Tolerance

High-Deductible Plan G works differently from regular Plan G. The plan has the same general benefit structure as Plan G, but the plan does not begin paying until you meet the annual high deductible. For 2026, that deductible is $2,950. Before that deductible is met, Medicare still pays its share, but you are responsible for your share of Medicare-approved costs up to the deductible.

The main appeal of High-Deductible Plan G is the premium. It can be dramatically lower than regular Plan G or Plan N. The risk is that you may have meaningful out-of-pocket costs in a year when you use care. This plan can be attractive for people who are healthy, have adequate savings, and want to protect against larger Medicare-approved expenses while keeping monthly premiums low.

| High-Deductible Plan G Works Best When… | Be Careful If… |

| You want the lowest possible Medigap premium | You would be uncomfortable paying the annual deductible in a bad health year |

| You rarely use medical care | You expect regular outpatient procedures, tests, or therapies |

| You have emergency savings | You want nearly zero surprise bills |

| You understand the deductible resets each year | You are choosing it only because someone marketed it as “same as Plan G” without explaining the deductible |

High-Deductible Plan G is not bad; it is just different. It should be chosen intentionally, not accidentally. For the right person, it can be an efficient way to combine Original Medicare flexibility with a low monthly premium. For the wrong person, it can feel frustrating because the plan may not pay anything until significant costs have accumulated.

Decision Guide: Which Medigap Plan Fits You?

There is no single best Medigap plan for everyone. A retiree who sees several specialists and wants no networks may reasonably choose Plan G. A healthy person who sees a doctor once or twice a year may prefer Plan N. A person with strong savings and a premium-minimization mindset may consider High-Deductible Plan G. Use the following decision guide to narrow the choice.

| Question | If Your Answer Is Yes | Likely Direction |

| Do you want the most predictable out-of-pocket costs? | You want fewer surprise medical bills and less decision friction. | Plan G |

| Are you willing to accept small copays to lower premium? | You are comfortable with some bills and use care moderately. | Plan N |

| Do you rarely use medical care and want the lowest premium? | You can absorb the high deductible if needed. | High-Deductible Plan G |

| Do you travel often or split time between states? | You want provider flexibility without local networks. | Plan G or Plan N |

| Are you concerned about excess charges? | You want coverage for Part B excess charges where allowed. | Plan G |

| Is your main concern monthly cash flow? | You prefer lower fixed costs and accept more variable costs. | Plan N or High-Deductible Plan G |

Simple Medigap Decision Tree

- Do you want the most predictable costs after the Part B deductible? -> Choose Plan G.

- Are you comfortable with occasional doctor and ER copays to save premium? -> Compare Plan N.

- Are you healthy, rarely use care, and comfortable with a $2,950 deductible in 2026? -> Consider High-Deductible Plan G.

- Are you unsure or comparing close rates? -> Compare actual premiums, household discounts, and company stability in your ZIP code before choosing.

How Much Do Medigap Plans Cost in 2026?

Medigap premiums vary widely. Your cost depends on your state, ZIP code, age, gender where allowed, tobacco status where allowed, household discount eligibility, plan letter, company, and sometimes application timing. Two people in different ZIP codes can pay very different rates for the exact same plan letter. Two companies in the same ZIP code can also charge very different premiums for identical standardized benefits.

The following ranges are broad estimates, not a substitute for ZIP-code-specific quoting. They are included to help you understand relative pricing.

| Plan | Typical Monthly Premium Pattern | Cost Predictability |

| Plan G | Usually higher than Plan N and HDG | Highest among commonly chosen plans |

| Plan N | Usually lower than Plan G | High, but copays and excess charges may apply |

| High-Deductible Plan G | Usually lowest premium | Lower until deductible is met; then similar to Plan G |

| Plan F | Often highest if available | Very high, but not available to newly eligible Medicare beneficiaries after 2020 |

The 2026 Medicare Part B premium and deductible are separate from your Medigap premium. CMS announced that the standard Part B premium for 2026 is $202.90 per month and the Part B deductible is $283. These Medicare costs matter because Plan G and Plan N do not cover the Part B deductible. You can confirm current Part B amounts through the official CMS 2026 Medicare Parts A and B premiums and deductibles fact sheet.

Why Medigap Rates Vary So Much

Because Medigap benefits are standardized, rate differences can be surprising. But each insurance company sets its own premiums and can use different pricing assumptions. Companies may price differently based on claims history, age mix, growth strategy, state rules, discounts, and how aggressively they want to compete in a specific market.

| Pricing Factor | How It Can Affect Your Premium |

| ZIP code | Rates can differ by county or rating area. |

| Age | Attained-age policies generally increase with age; issue-age and community-rated structures work differently. |

| Gender | In many states, male and female rates differ. |

| Tobacco status | Some states and companies charge more for tobacco use; some open enrollment rules limit this. |

| Household discount | Some companies offer meaningful discounts if someone else lives in the household or also has coverage. |

| Company rate strategy | Some carriers enter markets low and later adjust rates; others price more conservatively. |

| Underwriting class | If applying outside open enrollment, health status can affect approval and sometimes rating. |

Tobacco pricing is especially state-specific. Some companies or states treat tobacco differently during the initial enrollment window, while others apply tobacco rates more broadly. If tobacco status is relevant to your situation, it should be considered when you request Medigap quotes because it can change which company is most competitive.

Issue-Age, Attained-Age, and Community-Rated Medigap Pricing

Medigap pricing methods are often misunderstood. A plan’s pricing method does not automatically tell you whether it will be the best long-term value. State rules, company pricing, and actual rate increase history matter more than the label alone. Still, understanding the terms is useful.

| Pricing Method | Basic Meaning | Important Caution |

| Attained-age rated | Premium is based on your current age and may rise as you get older. | This is common; rate increases can also happen for other reasons. |

| Issue-age rated | Premium is based on your age when the policy is issued. | It may still increase due to inflation, claims, or class adjustments. |

| Community-rated | People in the same rating area generally pay the same regardless of age. | This does not mean premiums never increase. |

A common mistake is assuming issue-age automatically beats attained-age. That is not always true. A higher-priced issue-age plan can still cost more over time than a lower-priced attained-age plan, depending on actual increases. The better analysis is to compare current premium, expected rate behavior, company history, and state-specific pricing rules together.

Medigap Rate Increases: What to Expect Over Time

Medigap premiums are not locked forever. Even though your policy is guaranteed renewable as long as premiums are paid, rates can increase. Rate increases may happen because of age, company-wide rate adjustments, inflation, claims experience, or changes to Medicare cost-sharing.

Many people receive a Medigap premium increase letter around their policy anniversary or birthday month, though timing varies by company and state. If you receive an increase, do not panic and do not automatically cancel your policy. First, calculate the dollar increase, the percentage increase, and how your new rate compares with other companies offering the same plan. The guide on how much Medigap premiums increase each year explains why increases happen, and the breakdown of Medigap premium increase letters shows how to read the notice.

| When Your Rate Goes Up | What to Do |

| Small increase | Compare it with inflation and the company’s past behavior; it may not require action. |

| Large increase | Shop the same plan letter with other companies if you can pass underwriting or qualify for a special rule. |

| Repeated increases | Review long-term company stability and whether another carrier is better positioned. |

| Increase after health changes | Be cautious; switching may require underwriting in most states. |

| Increase during birthday-rule eligibility | Check whether your state allows a no-underwriting switch. |

When Can You Enroll in a Medigap Plan?

The best time to buy a Medigap plan is usually your Medigap Open Enrollment Period. Under federal rules, this is a six-month period that starts the first month you are both age 65 or older and enrolled in Medicare Part B. During this window, you can buy any Medigap plan sold in your state without medical underwriting.

This is different from the Annual Enrollment Period in the fall. The fall Annual Enrollment Period is mainly for Medicare Advantage and Part D changes. It is not an annual Medigap open enrollment period in most states. That distinction is one of the most important points in Medicare planning. The full explanation of Medicare Supplement Open Enrollment is worth reading before you delay or assume you can easily change later.

| Enrollment Window | What It Means for Medigap |

| Medigap Open Enrollment | Best window; generally no health questions or denial. |

| Annual Enrollment Period | Usually not a Medigap open enrollment period; applies mostly to Part D and Medicare Advantage. |

| Guaranteed Issue Period | Special rights in specific situations, but plan choices may be limited. |

| Birthday rule / state switching rule | Available in some states; details vary significantly. |

| Regular application after open enrollment | Medical underwriting usually applies in most states. |

Medicare also explains that the Medigap Open Enrollment Period starts when you have Medicare Part B and are 65 or older. While Medicare itself has no oversight of the Medigap plans and is not always an accurate resource for Medigap rates, the official Medicare.gov Medigap buying guidance is a helpful source for confirming the basic federal rule.

Medical Underwriting: Why Your First Medigap Choice Matters

Outside of Medigap Open Enrollment or a special guaranteed issue situation, most people who want to switch Medigap plans or companies must answer health questions. This is called medical underwriting. The insurance company can review your health history, prescriptions, height and weight, recent procedures, pending tests, and diagnoses before deciding whether to approve the application.

That is why your first Medigap decision matters. You may be able to change later, but you should not assume you can change easily. Some people can qualify for a lower premium later. Others develop health conditions that make switching difficult. The full guide to medical underwriting for Medigap plans explains how this process works and why company-specific rules matter.

| Underwriting Consideration | Why It Matters |

| Recent hospitalizations | Can trigger declines or waiting periods depending on company rules. |

| Pending tests or surgeries | Often a major underwriting issue because outcomes are unknown. |

| Cancer, heart disease, COPD, diabetes complications | Rules vary, but these conditions can affect eligibility. |

| Prescription history | Carriers often review medications as part of underwriting. |

| Height and weight | Build charts can affect approval with some companies. |

| State rules | Some states provide additional switching rights that reduce underwriting barriers. |

Guaranteed Issue Rights: When You May Have Special Medigap Protection

Guaranteed issue rights allow you to buy certain Medigap plans without medical underwriting in specific situations. Common examples include losing certain employer or retiree coverage, moving out of a Medicare Advantage service area, a Medicare Advantage plan leaving your area, or trying Medicare Advantage for the first time and returning to Original Medicare within a limited trial period.

Guaranteed issue is valuable, but it is not identical to open enrollment. In many situations, your available plan choices may be limited. The rules also vary by timing and situation. If you think you may have a guaranteed issue right, review when a Medicare Supplement is guaranteed issue before submitting an application or canceling existing coverage.

| Open Enrollment | Guaranteed Issue |

| Usually applies when you first start Part B at age 65 or older | Applies only in specific qualifying situations |

| Generally lets you choose any Medigap plan sold in your state | May limit which plan letters are available |

| No medical underwriting | No medical underwriting for eligible guaranteed issue choices |

| Best broad protection window | Important safety net, but narrower than open enrollment |

Birthday Rules and State Switching Rights

Some states have special rules that allow Medigap policyholders to switch plans or companies without normal medical underwriting during a certain annual window. These rules are often called “birthday rules,” but the details vary substantially by state. Some allow equal or lesser benefit changes. Some limit the window to a birthday period. Some apply around policy anniversaries. Some require staying with the same company or switching to a like plan.

This is one of the reasons Medigap advice should not be generic. A strategy that works in California, Oregon, Nevada, Missouri, or another birthday-rule state may not apply in a state without that rule. The overview of Medigap birthday rule states should be treated as a companion page to this guide because it changes the long-term flexibility analysis.

| State Rule Type | How It Can Affect Your Decision |

| Birthday rule | May allow a no-underwriting switch around your birthday, usually with restrictions. |

| Anniversary rule | May allow a change around the policy anniversary instead of birthday. |

| Guaranteed issue expansion | Some states give rights beyond federal minimums. |

| Unique plan standardization | Massachusetts, Minnesota, and Wisconsin use different structures. |

| Under-65 disability rules | Availability and price for disabled beneficiaries under 65 vary by state. |

State-Specific Medigap Rules: Why Your ZIP Code Matters

Medigap is federally standardized in most states, but state rules still matter. Your state can affect plan availability, pricing method, birthday-rule eligibility, under-65 disability options, tobacco rules, excess charge exposure, and which companies are competitive. Your ZIP code can affect premium even within the same state.

Three states do not use the standard Medigap letter system in the same way as most other states: Massachusetts, Minnesota, and Wisconsin. If you live in one of those states, the normal Plan G / Plan N conversation needs to be translated into that state’s structure. You can review the state-specific explanation of Minnesota Medigap plans and the Wisconsin article explaining why Wisconsin Plan G does not exist under that name for examples of how state rules change the comparison.

As a North Carolina-based independent agency, 65Medicare.org also maintains a detailed guide to North Carolina Medigap plans because local rules, carrier competitiveness, and pricing patterns matter. For people in states with special rules, pages such as the Nevada Medicare Supplement birthday rule and Pennsylvania Medigap plans can support more specific decisions.

| State-Specific Issue | Example of Why It Matters |

| Pricing method rules | Some states restrict or influence how companies rate policies. |

| Birthday rules | Can allow future switching without underwriting. |

| Excess charge rules | Some states limit or prohibit Part B excess charges. |

| Under-65 disability access | State rules determine availability and affordability for many disabled beneficiaries. |

| Unique standardization | MA, MN, and WI require a different comparison method. |

| Carrier competitiveness | The best-priced company in one state may be uncompetitive in another. |

Part B Excess Charges and Foreign Travel Emergency Coverage

Medicare Part B excess charges can occur when a provider does not accept Medicare assignment and charges more than the Medicare-approved amount, subject to Medicare limits. Plan G covers Part B excess charges. Plan N does not. In many cases, excess charges are not a major issue, but they can matter depending on your providers and your state. The explanation of Medicare Part B excess charges gives more detail on when this matters.

Foreign travel emergency coverage is another feature that can influence plan choice. Several Medigap plans include limited foreign travel emergency benefits, typically paying 80% after a deductible up to plan limits. This is not the same as comprehensive international health insurance, but it can be meaningful for people who travel. If international travel is part of your retirement, review whether Medicare covers you outside the country before assuming your Medicare coverage follows you overseas.

| Feature | Plan G | Plan N | Why It Matters |

| Part B excess charges | Covered | Not covered | May matter with providers who do not accept assignment in states where excess charges are allowed. |

| Foreign travel emergency | 80% up to plan limits | 80% up to plan limits | Useful for some international travel, but not a substitute for full travel medical coverage. |

| U.S. provider access | Any provider accepting Medicare | Any provider accepting Medicare | No Medicare Advantage-style network restrictions. |

Medigap for People Under 65 on Medicare Disability

Most Medigap conversations focus on people turning 65, but some people qualify for Medicare earlier due to disability. Medigap access for people under 65 is highly state-specific. Federal law does not require every state to offer the same Medigap protections to beneficiaries under 65, so availability, plan choices, and premiums vary widely.

A person under 65 may have fewer choices and higher premiums than someone turning 65. However, when that person later turns 65, they generally receive a new Medigap Open Enrollment Period tied to being 65 and enrolled in Part B. The guide to Medicare Supplement plans for disabled beneficiaries under 65 provides a state-by-state starting point for this issue.

Medigap vs Medicare Advantage: The Bigger Decision

Before choosing Plan G, Plan N, or High-Deductible Plan G, make sure you have chosen the right overall Medicare path. The first decision is not “which Medigap plan?” The first decision is whether you want Original Medicare with a Medigap plan and Part D, or whether you want Medicare Advantage.

| Decision Point | Original Medicare + Medigap | Medicare Advantage |

| Provider access | Any provider that accepts Medicare | Usually network-based |

| Referrals | Generally no referrals required by the supplement | May require referrals depending on plan |

| Prior authorization | Typically less plan-based authorization for Medicare-covered services | Often more prior authorization |

| Premium structure | Higher monthly supplement premium | Often lower premium |

| Out-of-pocket structure | More predictable with Plan G/N/HDG | Copays and annual max out-of-pocket apply |

| Annual changes | Medigap benefits are standardized and guaranteed renewable | Plan benefits, networks, and drugs can change annually |

| Switching later | May require underwriting to get Medigap | Annual election periods apply for Advantage changes |

Medicare Advantage can be a good fit for some people, especially those comfortable with networks and managed-care rules. But it is not the same as Medigap. If you start with Medicare Advantage and later want a Medigap plan, you may need to pass medical underwriting unless you are within a trial right or another guaranteed issue situation. That is why the Medigap vs Medicare Advantage comparison should be read before making the first-year decision.

How to Choose the Best Medigap Insurance Company

Since the benefits are standardized, the best Medigap insurance company is usually not the company with the flashiest marketing. It is the company that offers the best combination of premium, stability, discount eligibility, underwriting fit, and state-specific competitiveness for the plan you want.

| What to Compare | Why It Matters |

| Premium for the same plan letter | The same coverage can cost dramatically different amounts. |

| Household discount | A discount can change the ranking of companies. |

| Rate increase history | Low first-year premium is less helpful if increases are unusually aggressive. |

| Financial strength / reputation | You want a company with a stable presence and reliable administration. |

| Application timing | Some companies allow applications earlier than others. |

| Underwriting flexibility | Important if you are switching later or applying outside open enrollment. |

| State competitiveness | A company strong in one state may not be strong in another. |

Using an independent Medicare broker can help because a true independent broker can compare multiple companies in one place. The premium is generally the same whether you use a broker or go directly to the insurance company, but a broker can help you avoid choosing a high-priced company for identical benefits.

Real-World Medigap Decision Examples

| Situation | Likely Best Starting Point | Why |

| Turning 65, wants maximum predictability | Plan G | Simple structure and broad standardized coverage. |

| Healthy, few doctor visits, wants lower premium | Plan N | Premium savings may justify occasional copays. |

| Healthy, high savings, very premium-sensitive | High-Deductible Plan G | Lowest monthly premium with higher deductible risk. |

| Splits time between two states | Plan G or Plan N | Original Medicare + Medigap works well for snowbirds because there are no local networks. |

| Concerned about future ability to switch | Plan G or carefully selected Plan N | First choice matters because underwriting may apply later. |

| Currently on Medicare Advantage and wants Medigap | Depends on guaranteed issue or underwriting | May need to qualify medically unless a special right applies. |

Snowbirds and frequent travelers should pay particular attention to provider access. Medigap’s ability to work with any provider that accepts Medicare is one of its most important advantages over many Medicare Advantage arrangements.

Common Mistakes When Comparing Medigap Plans

| Mistake | Better Approach |

| Choosing a company because of brand recognition only | Compare rates and stability for the same standardized plan. |

| Assuming all fall open enrollment periods apply to Medigap | Understand that Medigap usually has its own one-time open enrollment window. |

| Picking the lowest premium without checking discounts and rate history | Look at value, not just the first-year rate. |

| Choosing Plan N without understanding excess charges and copays | Compare total expected costs and provider patterns. |

| Choosing High-Deductible Plan G without understanding the deductible | Make sure you can absorb the deductible in a high-use year. |

| Waiting too long to enroll | Protect your open enrollment rights and avoid underwriting if possible. |

| Assuming you can switch anytime with no health questions | Most states require underwriting outside protected windows. |

Step-by-Step: How to Compare Medigap Plans the Right Way

- Confirm that you are enrolled in Medicare Part A and Part B, or know your future effective dates.

- Decide whether you want Original Medicare with Medigap and Part D or Medicare Advantage.

- Compare Plan G, Plan N, and High-Deductible Plan G based on your health usage and risk tolerance.

- Check your Medigap Open Enrollment Period or any guaranteed issue rights before applying.

- Review state-specific rules, including birthday rules, tobacco pricing, and under-65 disability protections if applicable.

- Compare real premiums by ZIP code for the same plan letter across multiple companies.

- Look at household discounts, rate history, and company stability.

- Enroll before your desired effective date and confirm your Part D coverage separately.

You can begin the practical comparison by requesting Medigap quotes by email and reviewing the rates side-by-side. Do not pick the first company that sends a mailer. Compare standardized benefits across multiple companies so you know what you are actually buying.

You can also view our turning 65 Medicare guide or view the turning 65 infographic below for information about how to pick the best plan.

Frequently Asked Questions About Medigap Plans

What is the best Medigap plan in 2026?

For many people turning 65, Plan G is the best starting point because it offers the most comprehensive coverage available to newly eligible Medicare beneficiaries after the Part B deductible. However, Plan N may be a better value for someone willing to accept copays and no excess-charge coverage in exchange for a lower premium. High-Deductible Plan G may fit someone who wants the lowest premium and can tolerate the annual deductible risk.

Is Plan G better than Plan N?

Plan G is more comprehensive than Plan N because it does not have Plan N-style office visit or emergency room copays and it covers Medicare Part B excess charges. Plan N can still be a better value when the premium savings are large enough and the person is comfortable with those tradeoffs.

What is the downside of Plan N?

The main downsides of Plan N are potential copays and no coverage for Part B excess charges. For someone who sees doctors frequently or wants maximum predictability, Plan G may be preferable.

What is the downside of High-Deductible Plan G?

The downside is that the plan does not begin paying until the annual high deductible is met. In 2026, the High-Deductible Plan G deductible is $2,950. The low premium is appealing, but the policyholder must be comfortable with more upfront cost exposure.

Do Medigap plans include prescription drug coverage?

No. Modern Medigap plans do not include outpatient prescription drug coverage. Most people who choose Medigap also enroll in a separate Medicare Part D plan.

Can I use Medigap anywhere?

Medigap works with Original Medicare. In general, you can use any doctor or hospital that accepts Medicare. That is one of the main reasons people choose Medigap over network-based coverage.

Can I be denied a Medigap plan?

During your Medigap Open Enrollment Period, you generally cannot be denied based on health. Outside open enrollment or a guaranteed issue situation, medical underwriting may apply in most states.

Can I switch Medigap plans later?

You can apply to switch later, but in most states you may have to pass medical underwriting unless you qualify for a birthday rule, guaranteed issue right, or other special state protection.

Are Medigap premiums the same from every company?

No. Benefits are standardized, but premiums vary by company, ZIP code, age, gender where allowed, tobacco status where allowed, discounts, and state rules.

Is Medigap better than Medicare Advantage?

Not always, but Medigap generally offers broader provider flexibility and more predictable cost-sharing. Medicare Advantage often has lower premiums but uses plan networks, copays, prior authorization, and annual plan changes. The right choice depends on your priorities.

Does Medigap cover dental, vision, or hearing?

Standard Medigap plans do not usually cover routine dental, vision, or hearing services. Some insurance companies may offer separate ancillary plans, but those benefits are not part of standardized Medigap coverage.

Does Medigap cover foreign travel?

Some Medigap plans include limited foreign travel emergency coverage up to plan limits. It is not the same as complete international travel medical insurance, so frequent international travelers should review the details carefully.

Do I need a broker to buy a Medigap plan?

You are not required to use a broker, but an independent broker can help compare rates from multiple companies. Since benefits are standardized, comparing price and company stability is usually more important than choosing based on advertising.

When should I compare Medigap plans?

If you are turning 65, you should usually start comparing several months before your Medicare Part B effective date. If you already have a Medigap plan, it is reasonable to compare options when your rate increases, but remember that underwriting may apply in most states.

Bottom line: How to Choose the Best Medigap Plan

The best Medigap plan is the one that gives you the right balance of coverage, predictability, premium, flexibility, and long-term value in your state. For most people, the starting comparison should be Plan G, Plan N, and High-Deductible Plan G. From there, the decision should be based on your comfort with risk, doctor usage, travel patterns, state rules, and real premium differences in your ZIP code.

Because Medigap benefits are standardized, you do not need to guess which company “covers better.” You need to compare the same plan letter across companies, understand the rules around enrollment and underwriting, and choose a company that is competitively priced and stable for your area.

If you want help comparing options, 65Medicare.org can provide a personalized list of rates and company ratings. You can request Medigap quotes by email or schedule a phone appointment to talk through the decision. You can also read client reviews to see how other Medicare beneficiaries describe the process.

____________________

65Medicare.org is a leading, independent Medicare insurance agency for people turning 65 and going on Medicare. We have worked with 15,000+ Medicare-eligible individuals over the last 18+ years, assisting with understanding and comparing the plans. You can contact us online or call us at 877.506.3378.

*Last Updated: May 13, 2026

*Sources Used: Medicare.gov, CMS.gov